Has Inflation Bottomed or Just Noise? Also a look into Labor Market Conditions

Has Inflation Bottomed or Just Noise? Also a look into Labor Market Conditions

Inflation Data

I have been saying for some time that various data prints, especially inflation related data, will oscillate over the next few months. I think this latest print is more likely to be an oscillation on a downward path than a new trend beginning.

First, a trend is not established with one data point. Also, inflation missing expectations does not necessarily indicate a new trend. For example, if we can state that 2023 was a year of disinflation, of the 12 months in that year looking at Core CPI 3 months missed expectations higher, 2 months missed expectations lower and the remaining months all came inline with expectations. That is to say, more months missed with hotter than expected inflation than cooler and yet the trend was still down.

To be clear, the core services data was troubling, as it will be for the Fed without question. Good disinflation remains an ongoing cooling input for CPI and I do not see that changing materially in 2024.

Housing makes up about 40% of Core CPI and I think we will see disinflation in that input going forward.

It should be noted that shelter related costs accelerated at a 0.6% m/m increase, and this category is a large component of CPI. However, given some of the alternative measures in this area are indicating that rents recently signed have actually stagnated in price levels, I am suspicious as to how sustainable this increase will be over the coming months. That is to say, I think it is more likely that rents will begin to disinflate than accelerate over the next few months.

Services is the big question, what will it take for services inflation to move lower? If a large component of services costs is labor, well that seems clear to me that the Fed will have to keep rates on hold for longer. This has been my thesis for quite a while, the economy, for the time being, is still too strong and the Fed will stay put. However where I differ among most strategists is that I do think the tight level of monetary policy will eventually lead to a broader slowdown and at that point rates will be cut by more than markets are currently pricing in. Again, I would not position myself anticipating rate cuts right now (ie. avoiding being long the front end) but ready to move once the data indicates the economy has begun to tilt to weakness.

A couple of weeks ago I wrote (article located here):

My concern is that historically when monetary policy is this restrictive, a recession usually occurs. The longer they keep rates this elevated, the higher the probability of a recession.

If the economy starts to crack, it is at that point that I think Fed cuts will be greater than the market expects.

If the economy holds steady, the Fed may continue to push out cuts further out in 2024.

Just quickly on PPI, core came in at 0.6% m/m, much stronger than expectations. Also note that last January core PPI also came in at 0.6%, however it was followed with a 0.3% February, and 0.1% March. One data point does not make a trend, so watching this data over the next few months.

It should be noted that 10 year breakevens are still contained. If the move higher in the 10 year is primarily due to the Fed cuts being priced out a couple of months and not as a result of higher long-term inflation expectations, in my opinion this would offer an attractive entry point. Obviously if inflation expectations move higher, this changes the situation. Given the move down in inflation so far and the emphasis the Fed has put forward regarding their intention to get inflation back to target, are institutions really doubting the Fed? I think this is a knee jerk reaction in markets, not a fundamental shift over the next decade.

Are We in Restrictive Territory?

We have to remember that inflation has fallen a lot over a short period of time. Coming down from over 9% y/y to just over 3% y/y is extraordinary, especially given that the economy has not contracted.

This also indicates to me that the level of monetary policy is indeed restrictive. This has been a topic among some people, that the economy may re-accelerate as they think we are not in restrictive territory.

I think the probability of a significant re-acceleration of economic activity is quite low for several reasons, including the latest survey of bank officers indicating that they continue to have tight lending standards. Also the very fact that inflation has decreased, along with a less tight labor market, also indicates that the overall pent-up demand is being subdued.

However, not everything moves in a straight line. Manufacturing has been in a decline for quite a while, yet there are some positive signs in this area. For example, last week the Philly Manufacturing Business Outlook Survey (report located here) diffusion index moved into positive territory for the first time since last August. However even that report is mixed with current shipments moving into positive territory but new orders remained negative (although rising) and firms reported a decline in employment.

Labor Market Conditions

Given that the labor market is the primary concern over potential inflationary escalation in the future, I wanted to take a look what is driving this pressure.

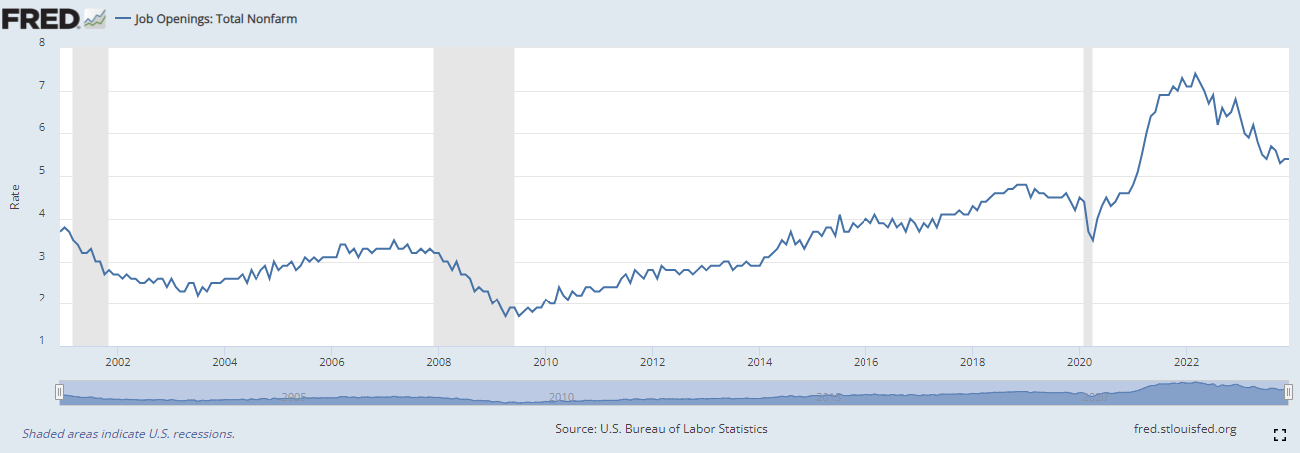

This is total nonfarm job openings. I know that job openings have taken criticism of late given how easy it is to post a job opening. Still, I don’t think that structural factors over the job posting market have changed materially over the last year or two (perhaps over the very long-term sure), over which time there has been a large decrease in openings. Not coincidental this is the same time period as the Fed has moved into monetary policy into restrictive territory (ie. Fed policy is working).

What is driving the economy now and why are job openings still above pre-covid levels?

With all of the discussion over food services and hotels, these are the job openings in this sector and they are below pre-covid levels.

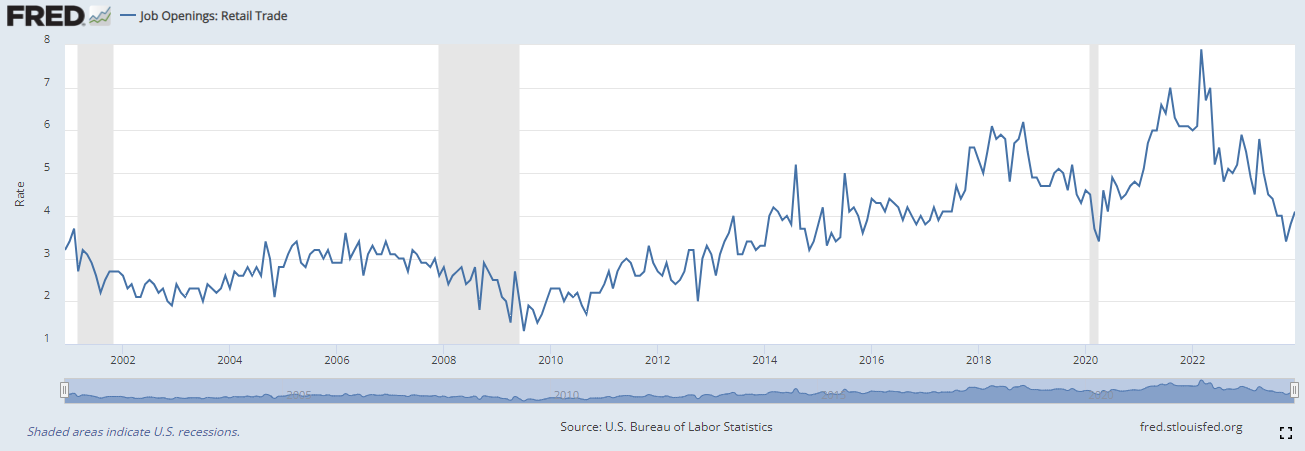

These are retail trade job openings, and no supply/demand imbalance is currently present here.

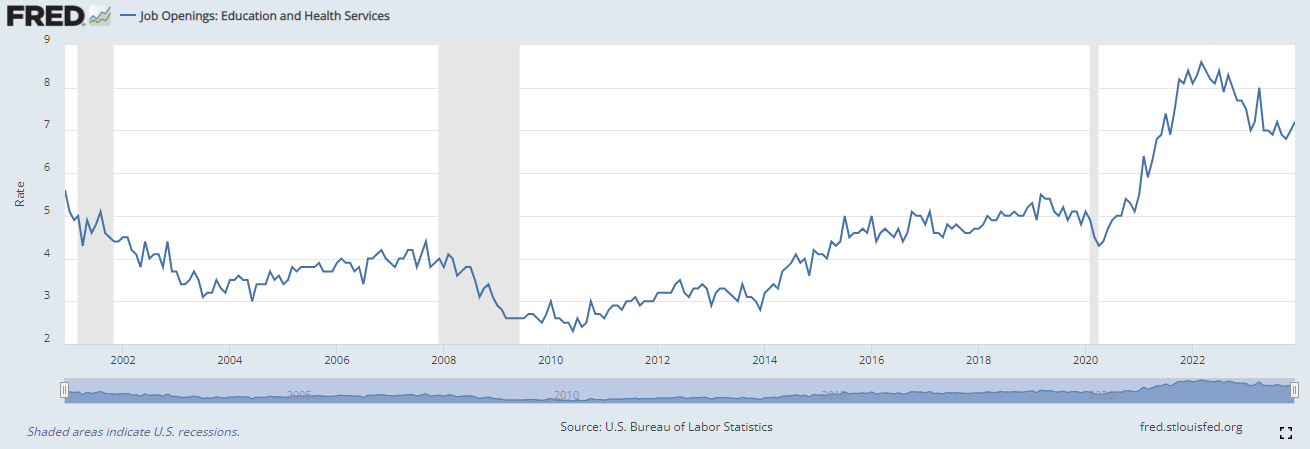

Here we are, education and health services still remains a strong sector.

Government is also an area of strong demand. (do we really want the government to be a large driver of jobs? that is for another day…..)

I think the quits rate is quite interesting. Here you will not get double counting like a job posting (ie. posting more than once for the same job). Total nonfarm quits rate is back to pre-covid levels. When one looks at the change from the recent high, it is quite a large decline, indicating a less easy market to get a new job and therefore fewer quits.

This is the quits rate for leisure and hospitality, again below pre-covid levels.

All of this is to say, I do not believe the economy is about to re-accelerate. Last week I discussed that delinquency rate on credit card loans is now above pre-covid levels, which is not usually a sign of an economy that is becoming stronger.

Consumer Sentiment

University of Michigan reported the latest consumer sentiment data. Sentiment was pretty much unchanged.

From the report (here),

“Consumers continued to express confidence that the slowdown in inflation and strength in labor markets would continue.

Year-ahead inflation inched up from 2.9 in January to 3.0% in February. For the second consecutive month, short-run inflation expectations have fallen within the 2.3-3.0% range seen in the two years prior to the pandemic. Long-run inflation expectations remained at 2.9% for the third straight month, staying within the narrow 2.9-3.1% range for 28 of the last 31 months.”

While inflation expectations have moved a touch higher, they really have not re-accelerated, which makes sense given the progress made over the past year on price pressures.

Also note the expectation by consumers in the report that the strength in labor markets will continue. Any cracks in the labor market and this would significantly change consumer sentiment, not to mention retail sales and other associated economy data.

Retail Sales

Retail sales came in much weaker than expected at -0.8% m/m vs expectations of -0.2%. Core retail sales also were much weaker at -0.6% m/m vs expectations of a gain of 0.2%.

As I am sure everyone knows, retail sales are not inflation adjusted, so these are very weak numbers.

A few interesting items in this report. First, some people were saying weather had an effect on the data, but if that is the case why were online retailers down 0.8% m/m? Conversely, if the weather was so bad, why were food and drinking places up 0.7% m/m?

Interesting to also look at the m/m vs y/y data. For example, furniture and home furnishings were up 1.5% m/m, but still down 7.5% y/y. Perhaps the recent move down in yields has stimulated some activity around the home, but clearly the overall higher levels from a year ago are hurting this sector.

Since most Americans have jobs, they are still going out to eat and drink, although on a y/y basis at 2.5%, when one considers the level of inflation over this past year it is not significantly strong. However, the tight level of monetary policy will continue to be a drag on retail sales going forward, especially large discretionary items.

Crowded Positioning

There has been some interesting data on positioning lately, all of which is leading me to raise an eyebrow at the potential opportunity if sentiment shifts. The Bank of America monthly global fund manager survey was out and the number of managers expecting a recession has turned negative for the first time since April of 2022. Just 11% expect a hard landing. The most crowded trade is to be long the Magnificent Seven, with the second most crowded trade being short Chinese equities (I discussed a trading idea on Chinese equities last week, article here).

What I like to see is when positioning is leaning very heavily one way, usually when markets are not incorporating the probability of an event to the same degree as I believe is appropriate. Not that I would trade against the crowd before data indicates a change, but that I am thinking about alternative possibilities and waiting to pounce. This is when the markets move the most, as market participants adjust positioning when data suggests their base case might be incorrect.

So far, earnings season and the economy are holding up, but I think that will not last all year long. Again, I was long equities going into this week (more on that below), but cautious and always on the lookout for when sentiment can shift.

Earnings Season

Normally I like to focus on the macro/big picture not the individual story. However, just to highlight what I mentioned above regarding consumers (and last week with credit cards), there really is a bifurcated economy between those well-off (usually that refers to consumers with a stock portfolio) and those not well-off.

McDonald’s quarterly earnings call was last week and commentary from the CEO, Christopher Kempczinski, was quite interesting. On the call he stated, “…where you see the pressure with the U.S. consumer is that low-income consumer. So call it $45,000 and under. That consumer is pressured. From an industry standpoint, we actually saw that cohort decrease in the most recent quarter, particularly I think as eating at home has become more affordable. There's been much less pricing that's been taken more recently on packaged food. So you're seeing that eating at home is becoming more affordable that I think is putting some pressure from a IEO standpoint on that low-income consumer.

If you think about middle income, high income, we're not seeing any real change in behavior with those. We continue to gain share with those groups. But the battleground is certainly with that low-income consumer.”

There are cracks forming, and while they may be in the lower income demographic for now, if the Fed really wants to squeeze inflation out of the economy they will need to keep monetary policy restrictive, and that will continue to be a drag on the economy. Given the low level of unemployment, to see that the lower-income consumer is really shifting away from McDonald’s and changing their consumption is quite interesting. What will happen to sales if the economy really starts to slow and the unemployment rate increases? (rhetorical question)

So far 79% of S&P 500 companies have reported so far this earnings season. The earnings growth rate is running at 3.2%. Next week quite a few retailers will be out, this will be important to watch and see what they say about their business and forward guidance.

The 12 month forward P/E is 20.4, which is not cheap. I have been saying that for some time, but P/E is not a timing tool of course and as such I have not been short but long as capital flows are more important over the short-term.

So far the data is reasonably strong, but I think it is interesting to note that firms reporting positive earnings surprises are only 1.2% above estimate, below both the 5 and 10 year averages.

For the entire 2024 year, analysts are expecting a strong increase of 10.9% in earnings. That seems optimistic to me if the Fed will keep rates elevated for longer. A lot of things have to go right without hiccups for analysts to be correct (ie. soft landing is required).

What to Watch This Week

Wed FOMC minutes

While the Fed minutes will most likely outline the discussion over rate cuts, the recent inflation data will make some of these talking points stale. Still, it will be interesting to better understand how the Fed was thinking about monetary policy at that time, including discussion over QT

Weekly unemployment claims and flash PMI data

Equities

After a long period of time being long from 4400, I finally closed the last of my position on this gap lower day, as it hit my trailing stop targets (discussed last week).

For the time being I will be flat, but I am watching equities closely. First, if yields are backing up, it would make sense for equities to sell-off. Second, the momentum in stocks is starting to wane. Notice that relative strength is failing to make higher highs, unlike the S&P 500. This is not a “magic” trading signal, just a sign that the underlying momentum is slowing down and this could result in selling pressure. A lot of people have made quite a bit of money lately and if selling pressure begins, it could create even more sales. The 4920 area is important to watch. I would enter a small short position if the SPX enters that area but anticipate some back and forth trading in the 4860-4920 range. Either I am wrong and the market reverses higher (stops near and slightly above recent highs), or others begin to think about taking some money off the table and more selling pressure ensues. At the very least I would put on option trades to profit from a move lower.

Fixed Income

As I still think that the Fed’s restrictive monetary policy will result in an economic slowdown later this year, and I also think fund managers will be looking to buy the dips in longer duration assets. I added a little to the longer end of the curve, specifically the 10 year. I don’t think much will change this week, as there is little top tier economic data. As I discussed last week, I also added more to longer duration ETFs in my retirement accounts, selling calls along with the long to generate higher yields. I don’t think yields will drop immediately down (which is when you do not want to sell covered calls, if a large move is anticipated).

I think we might have to wait until March to see if the economy is slowing down, or re-accelerating. Obviously if February and March come in even hotter in terms of inflation and jobs I would re-evaluate my positioning. But the real pain would be in the front end of the curve if that occurred, as the Fed would then have to consider raising rates. A small probability, but not zero.

Ultimately I think the Fed will get inflation back to target over time (ie. they will not increase the target level), although given history there is a high likelihood that a recession will also be part of this process.

Oil

After quite a bit of back and forth trading, it seems like oil is ready to move higher. I would go long WTI (this is the daily continuous chart) anywhere up to $77.80, looking for an initial profit taking zone in the $83-$83.25 level and stops in the $74.50-$75 region. If WTI can get through the $83.50 the next level of resistance I think would be in the $88 region.

Gold

I was long gold in the $2020 region, as I wrote in the last research report “Last week was not a very convincing week for someone holding a small long position. I did put on a very small position and am moving my stop to just under $2020.” I did close my position at pretty close to flat. There appears to be little in terms of direction so I am sitting on the sidelines.

Thanks for reading!

theglobalmacrotrader@gmail.com

Twitter —> @TheGlobalMacro

Disclaimer

Copyright (c) TheGlobalMacroTrader.com 2024. All rights reserved. All material presented either through the TheGlobalMacroTrader.com website, Substack, any newsletter published by this site, posts on any social media platform and other public comments are not to be regarded as investment advice, but for general informational and entertainment purposes only. You, the reader, assume the entire cost and risk of any trading you choose to undertake. You, the reader, are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice and are for entertainment purposes only, no advice has been presented and no recommendation have been made. All information on TheGlobalMacroTrader.com, and any associated pages such as the SubStack pages, are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings along with discussion over chart formations and quantitative metrics may be mentioned but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security—including commodities, currencies, stocks, bonds, exchange traded funds (ETF), exchange traded notes (ETN), mutual funds, futures contracts, or any similar instruments. All text, images, ideas and concepts on TheGlobalMacroTrader.com and associated websites, emails, posts and social media messages constitute valuable intellectual property. No material from any part of TheGlobalMacroTrader.com and associated websites, emails, posts and messages may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of TheGlobalMacroTrader.com. All unauthorized reproduction or other use of material from TheGlobalMacroTrader.com and associated websites, pages and emails shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. The recipient should check any email and any attachments for the presence of viruses. TheGlobalMacroTrader.com accepts no liability for any damage caused by any virus transmitted by this company’s website, emails, attachments, posts and any other method of communication. TheGlobalMacroTrader.com expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. TheGlobalMacroTrader.com reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.