5 Topics Covered This week 1) The Consumer, 2) Auctions, 3) Fed Speakers, 4) Commercial Banking, and 5) China

Senior Loan Officer Survey & the Consumer

The January survey was released last week (report is located here). 85% of respondents stated credit conditions are unchanged. The Fed could take this as a positive in the sense that banks are not putting their foot down further as a result of stress in commercial banking due to the New York Community Bancorp situation. However, standards remain tight, this is still creating a drag on the economy.

One area I want to highlight is regarding the special questions over the banks’ expectations for changes in 2024.

An excerpt from this section:

“Banks, on balance, reported expecting lending standards to remain basically unchanged for C&I (commercial and industrial) and RRE (residential real estate) loans, but to tighten further for CRE (commercial real estate), credit card, and auto loans. In addition, banks reported expecting loan demand to strengthen across all loan categories, and loan quality to deteriorate across most loan types.”

So, banks expect to tighten credit card, auto loans and CRE, along with expectations of loan quality to deteriorate across most loans, yet loan demand is expected to strengthen - why? “The most frequently cited reason for stronger loan demand over 2024, reported by a major net share of banks, was an expected decline in interest rates.”

There is ongoing pain as loan quality is deteriorating and lending standards remain tight, but customers are optimistic for one reason - they expect lower rates. How does this work if rates remain higher for longer? What if people and companies are expecting to refinance at lower rates and they cannot? (more on that below) This is where a potential issue arises, when realty differs from expectations.

Everyone keeps telling me the consumer is in “great” shape, can’t you tell from the last retail sales print? I would suggest 1) that print is backward looking and one has to take with a large grain of salt given the holiday season spending, and 2) there are many signs that the consumer is reaching a limit in terms of spending power.

Why do I say this? A few charts, courtesy of the St. Louis Fed:

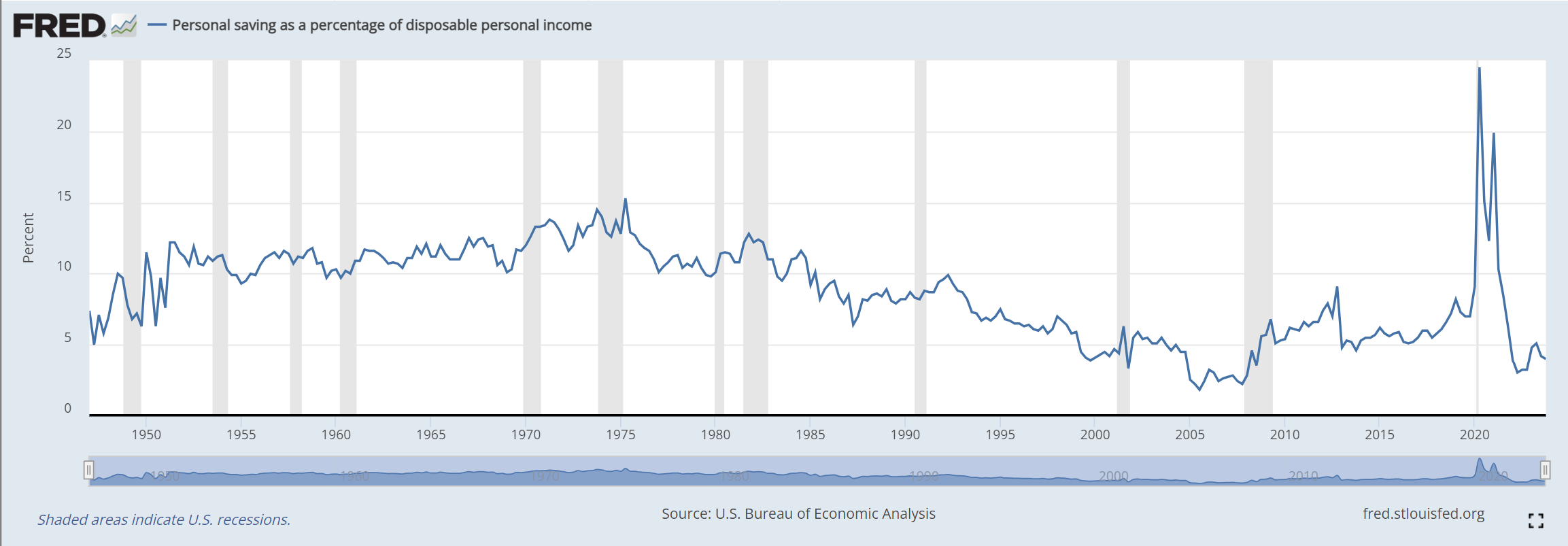

This is the personal savings rates as a percentage of disposable income. The current level is below pre-pandemic, and in fact one has to go back to 2007 to find a lower level. This is consistent with work conducted by the San Francisco Fed (post is located here) back in August of last summer (I discussed it back then) in which they stated (emphasis mine),

“Overall, despite differing methodologies and assumptions, the existing body of work on household savings following the pandemic recession firmly points to the rapid accumulation and drawdown of excess savings in the United States. Our estimates suggest that a relatively small amount—around $190 billion—remains in the overall economy, and we expect the aggregate stock of excess savings will likely be depleted during the third quarter of 2023—that is, the current quarter—for which initial data will be released later.”

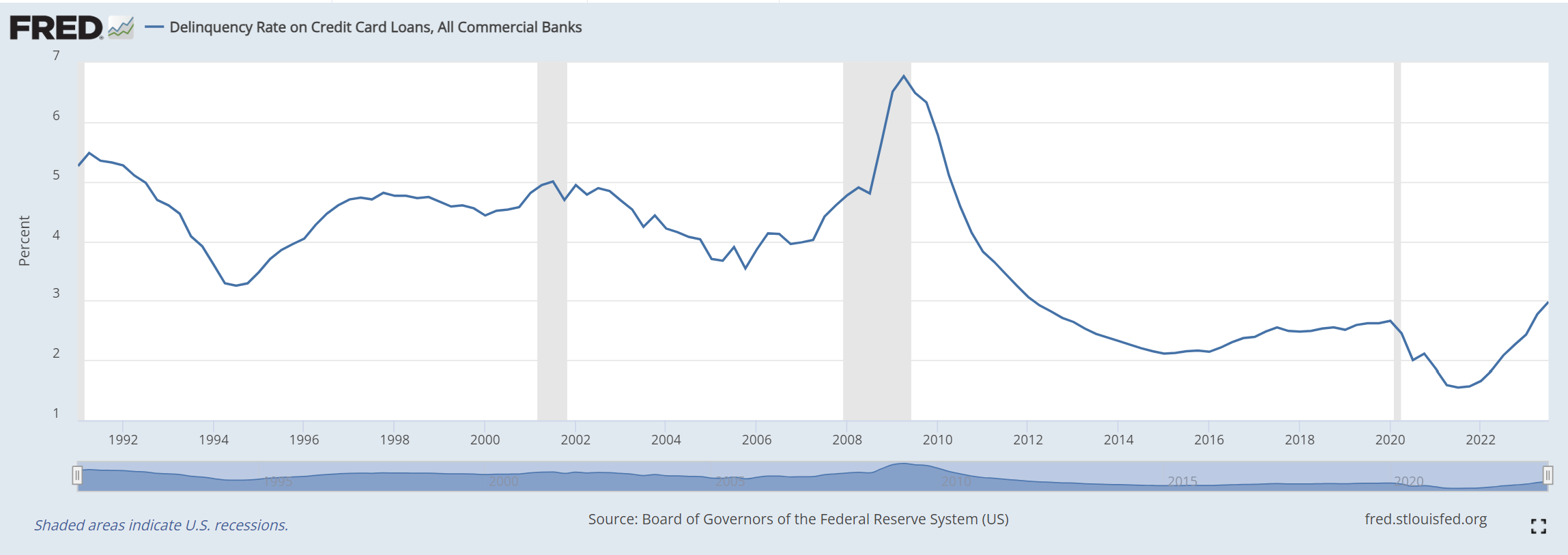

This makes sense to me, the decrease in consumer savings, given other data such as delinquencies:

This is the delinquency rate on credit card loans for all banks, now at higher levels than pre-pandemic.

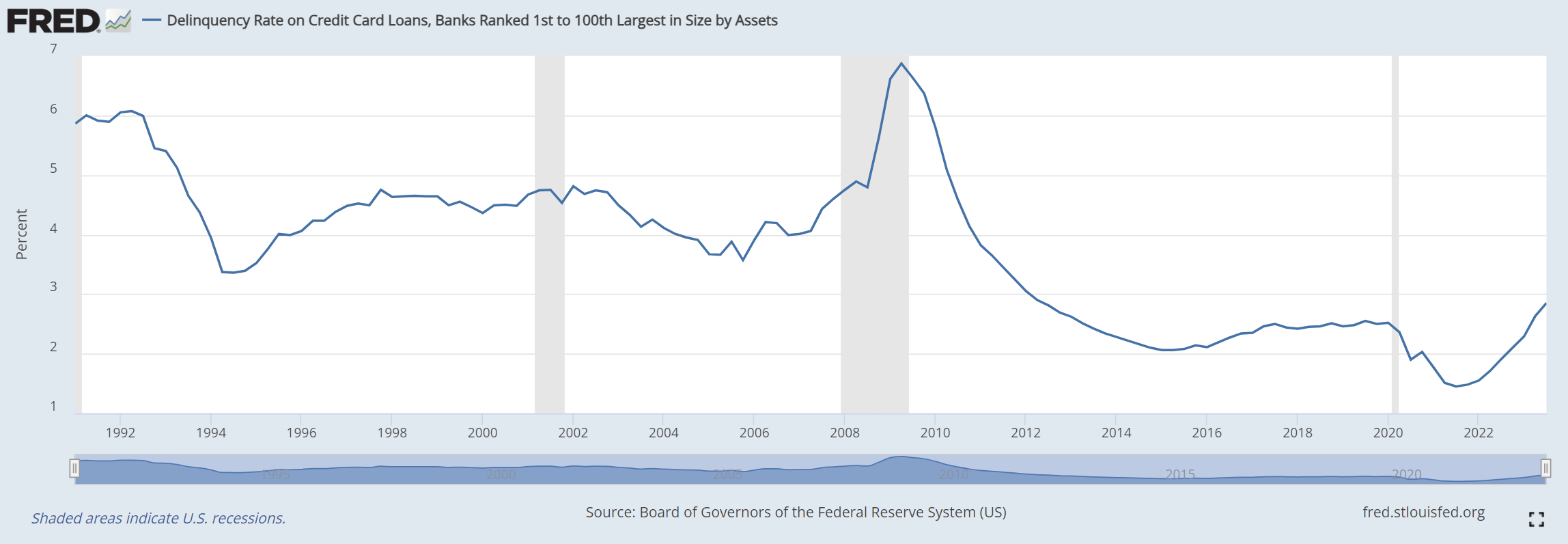

However, if one digs a little deeper, the market is really bifurcated between large and small banks:

This is the delinquency rate on credit card loans for the top 100 banks by assets.

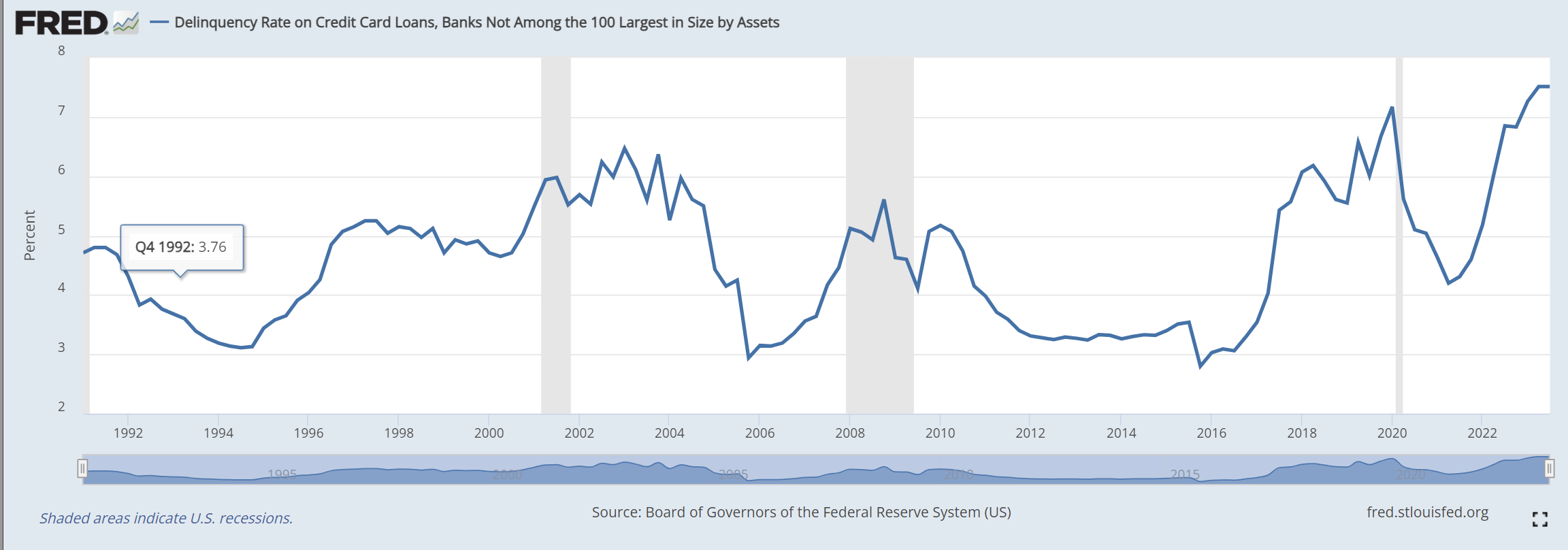

This is the delinquency rate on credit card loans for banks not in the top 100. While both are higher than pre-pandemic, for the smaller banks current credit card delinquencies are higher than the 2008/09 GFC and 2000 dot.com crash! This is not a picture of health for the consumer.

Why is there such a difference? I have to dig deeper to have higher confidence in my answer but an initial thought is that more affluent clients are with the top banks (including those located in major cities), while the smaller banks have less affluent clients. Also to consider, the affluent client has a larger portfolio of stocks, and stocks have done well this past year. The less affluent do not invest as much, or at all.

We know about the financial crisis last year, with SVB and so forth. That was driven from a lack of appropriate portfolio positioning and hedging against a move higher in rates, not from a significant increase in client delinquencies. Could there be another regional banking crisis, this time from client defaults? Potentially. It also lends support to the growing difference in performance from the top banks and regional banks, and perhaps the pairs trade between these two groups will still continue to work this year.

I would take caution from the argument that the consumer is in great shape. Signs of deteriorating will only be exacerbated if the unemployment rate increases, which I believe it will at some point this year.

Auction Results

Last week we had several auctions, with my eye to the benchmark 10 year. This was the largest 10 year note auction in history at $42 billion. I was concerned that the market would push yields back up with potential indigestion over such a large amount, but in fact it stopped through by 0.9bps along with more buyers from non-dealers (ie. investment funds that are price sensitive).

The Treasury department did state the size won’t increase, at least for the next several quarters. This gives some certainty as to 1) size of issuance, and 2) the end (most likely) of hiking rates, with the conversation over when rates will begin to be cut.

As a long-term fund manager, I can understand why there was good demand for this issuance. Sure, yields may back up somewhat, but I think the fundamental economic conditions would have to change substantially to get yields back up towards 5% again. Also, if you are a fund manager and missed out at 5%, and 4.50%, levels over 4% are looking increasingly attractive with a long time horizon. (more on this below)

Fed Speakers

There has been some talk that potentially the neutral rate, or r*, is higher than pre-pandemic. Last week Minneapolis Federal Reserve President Neel Kashkari stated, "It is possible, at least during the post-pandemic recovery period, that the policy stance that represents neutral has increased."

To be clear, while most on the Fed think that the neutral rate is 2.50%, or around that area, some think it is higher. The level higher, however, is not anywhere near current levels, but in the 3.50% region. That is to say, even if the Fed wanted to get back to an elevated “new” neutral level, it would still result in significant Fed cuts.

I believe this commentary is rationale to delay Fed cuts and squeeze inflation further, not a change in the Fed’s target of 2% as some have started whispering at this potential shift. I think the Fed knows that changing the target before they achieve it would blow their reputation to pieces and they will do everything possible to get back to 2%.

If there was to be a revisit of the 2% target, I do not think that would happen until late 2025 or 2026. changing the target ahead of reaching their objective would be admitting defeat. We know one thing, Chair Powell has referenced various prior Fed Chairs and their spot in history, he is worried about his legacy and therefore I think there is almost no possibility of changing the 2% target anytime soon (one can never say zero probability, because there is always some change, even if very small).

The resilience of the labor market is still a concern for the Fed, as discussed with the last jobs report. I think the Fed will keep rates as-is well into the second quarter, if the underlying economic data comes out as expected.

Commercial Banking

Treasury Secretary Yellen stated, at the Senate Banking Committee hearing, that the commercial real estate sector is a significant financial stability risk concern due to high vacancy rates and elevate borrowing costs, but does not believe it will end up being a systemic risk to the banking system. She did say that smaller banks may be stressed by these developments. Yellen also told the House Financial Services Committee that the situation was “manageable”.

While I like Yellen’s optimism, the track record of officials predicting the future is quite poor. The obvious example is the then-Fed Chair Bernanke in 2007 outlining the economic look in this speech (located here), with emphasis mine:

“Although the turmoil in the subprime mortgage market has created severe financial problems for many individuals and families, the implications of these developments for the housing market as a whole are less clear. The ongoing tightening of lending standards, although an appropriate market response, will reduce somewhat the effective demand for housing, and foreclosed properties will add to the inventories of unsold homes. At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.”

The topic over commercial real estate is not new, but more people are growing concerned. Commercial real estate is interesting in that it moves quite slow, but the overall size is huge. There is an estimated $1.2 trillion of debt that will mature through 2025 and require to be refinanced, with a total of $2.2 trillion due by the end of 2027. There was $6 trillion of outstanding commercial real-estate debt as of December 2023.

One of the big risks is that a large transaction (or several large deals) at lower prices causes everyone to mark-to-market their holdings down.

According to Fitch, delinquencies on commercial mortgages were 2.25% in 2023 but are set to rise to 4.5% this year and 4.9% in 2025.

Walking away from a property is looking increasingly like a good option. Investors in commercial real estate can just do so, especially when the debt exceeds the value of the asset. With higher interest rates, it lowers the valuation of an asset.

This was taken from a Morningstar article in December (located here). The longer rates remain elevated, the more stress there is for debt that matures and has to be refinanced. Given the size of this sector versus historical periods, we just don’t know what the effects will be of a significant increase in defaults. Could it cause risk-off across other sectors and markets? Quite possibly yes, as more parts of the economy are closely linked today versus years ago.

“Interest rates, pegged at 6.5% for commercial property loans in late December have eased back from above 7% this fall, but remain well above the pandemic lows of under 4%. The yield on the 10-year U.S. Treasury bond recently sunk to 3.87%, but remains much higher than the 1.4% range of two years ago.

That doesn't bode well as an estimated $1.2 trillion of commercial mortgage debt is set to mature through 2025, according to data from the Mortgage Bankers Association.

For years, owners of commercial real estate have pocketed billions of dollars by refinancing properties at skyrocketing values when debt was dirt cheap. As valuations come down, the debt attached to those properties is increasingly more than what the buildings are worth. The owners aren't expected to throw the money they have taken off the table down a sink hole now.

"In my mind, if you have anyone significantly underwater they may just want to hand the keys back," said Gabe Rivera, co-head of securitized products at PGIM Fixed Income, a division of PGIM, the $1.2 trillion asset management business of Prudential Financial Inc.

"No one is throwing good money after bad."

While no one knows what will occur in the future, given the massive amount of money we are talking about, I think this further strengthens the argument that adding fixed income duration on any large dips. Afterall, if the situation were to get out of control what would the Fed do? Drop rates significantly.

China

A very quick follow-up regarding China. I have been watching and waiting for the Chinese authorities to make a significant move in helping their economy and markets. I do realize that most Chinese citizens do not invest in equities, but given the long bear market in stocks combined with the falling real estate market, this is putting significant stress on the Chinese economy.

Last week, China replaced their head of the China Securities Regulatory Commission with Wu Qing, a former chairman of the Shanghai Stock Exchange, an unexpected move.

Chinese markets are closed this week for the Lunar New Year. The National People’s Congress begins on March 5th. The agenda will include national economic and social developments, along with central and local budgets.

I think there is a reasonable probability that Chinese leadership may put forward a significant plan to stem the downward slide in their equity and real estate markets. Will it be enough over the long-term? Probably not, but I think there is a decent probability that markets will move significantly over the next few months.

There are three potential scenarios:

Chinese equities do not move going into the summer. That seems like the least probable outcome. Given that Chinese leadership has started making changes already, albeit not well received so far, will they just stop now? Unlikely. I think the probability of Chinese equities being in a +-5% range from current levels is low.

Chinese equities sell off sharply. Markets are disappointed with current and potential future changes to stem the decline. (sell off being greater than 5%)

Chinese equities rally sharply. Markets are surprised by some future move and short sellers start to cover, this brings buyers into the market. (rally being greater than 5%)

Very difficult to call it perfectly, but I think either 2 or 3 are very likely to occur by the summer.

As a result of this thinking, I have started to put on option strategies that will benefit from a move either higher or lower from current levels, including straddles and strangles.

This is just one example, that being the iShares China Large Cap ETF (FXI). From the current price of 22.36, the market could rebound higher into the 29-34 area, or drop into the 16.50-18.75 area - either move would result in a profitable option trade if it occurs by the summer.

What to Watch This Week

CPI, expectations are for 0.2% m/m, and core 0.3% m/m. If the numbers come in as expected, that would result in y/y headline to be 2.8% and 3.6% core. Recall that goods disinflation has been doing the heavy lifting. If core services ex-housing remains strong, this will be a concern for markets and the Fed.

Retail sales, expectations are for a drop of -0.2% m/m for core and headline +0.1% m/m

PPI, 0.1% core and headline. PPI has been consistently low

Empire State Manufacturing, expectations are for improvement but a continued negative number at -11.9. Philly Fed Manufacturing Business Outlook Survey is also out this week.

Preliminary UoMichigan Consumer Sentiment

More Fed speakers, including Barkin

Equities

There is nothing new this week, so I will make this short and re-state from last week, “For the time being the short-term trade remains to be bullish equities” and “If momentum starts to regain, we could be setting up for a move towards 5300 or so.”

I still have an open position from 4400, and have continued to move my stop higher. This week is no exception, with stops now in the range of 4920-4930.

Fixed Income

This is the monthly 10 year yield, along with the effective Fed funds rate (black), the unemployment rate (red) and vertical lines indicating when the Sahm rule was triggered (ie. the unemployment rate exceeds 50bps of the relative bottom).

Why did I include this chart? I was asked if I thought the 10 year would back up even higher in yield, to above 5%. I think that is a low probability (albeit not zero). Why? I think 1) the economy is slowing down, and 2) inflation is also coming down. Under such a situation, if one waited until the unemployment rate really accelerated higher, they would have missed out on a nice move down in yields (the vertical red lines). As I have noted earlier, the consumer is starting to crack, although that appears to be the less affluent consumer. I think it is more likely that the unemployment rises at some point this year, given the level of restrictive monetary policy. I also think that inflation will continue to trend lower.

Given that the Fed themselves have rate cut expectations this year, not to mention the five 25bps cuts that markets expect, someone a year from now would most likely prefer the 10 year at over 4% yield versus what I believe will be a lower yield at that point in time. Could yields oscillate higher? Of course yes, but given the level of restrictive monetary policy, I would prefer to use history as a guide and not fight the Fed.

Last week I re-stated my prior view that, “I think we will see at least 3.50% at some point this year. I continue to look at trading ranges in the 10 year, buying in the 4.10-4.20% and looking to trim around 3.80%. I think there will be a few oscillations back and forth this year.”

As I think we will oscillate in ranges for most of this year, I will also (as I wrote about last week) have for my longer-term retirement account TLT and write calls against the position to generate even more yield.

Oil

I see no edge and no attractive risk:reward - I remain on the sidelines.

Gold

As I wrote last week, “I would want to see gold hold above $2020 or so for a few days and I would enter a small long. I would then add as gold moved through $2070-$2080.” Last week was not a very convincing week for someone holding a small long position. I did put on a very small position and am moving my stop to just under $2020. I would add more if gold moved above $2070 for some length of time (ie. not a quick spike over a few minutes) but this is a low conviction trade.

Bigger question, what is happening with gold miners?

This is the monthly chart of the VanEck Gold Miners ETF (GDX) versus the continuous gold contract (black). Very weak performance for gold miners. Are the gold miners trying to tell us something, or is the price of gold about to pull the miners back into life? I don’t know, but I do not like this type of divergence.

Thanks for reading!

theglobalmacrotrader@gmail.com

Twitter —> @TheGlobalMacro

Disclaimer

Copyright (c) TheGlobalMacroTrader.com 2024. All rights reserved. All material presented either through the TheGlobalMacroTrader.com website, Substack, any newsletter published by this site, posts on any social media platform and other public comments are not to be regarded as investment advice, but for general informational and entertainment purposes only. You, the reader, assume the entire cost and risk of any trading you choose to undertake. You, the reader, are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice and are for entertainment purposes only, no advice has been presented and no recommendation have been made. All information on TheGlobalMacroTrader.com, and any associated pages such as the SubStack pages, are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings along with discussion over chart formations and quantitative metrics may be mentioned but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security—including commodities, currencies, stocks, bonds, exchange traded funds (ETF), exchange traded notes (ETN), mutual funds, futures contracts, or any similar instruments. All text, images, ideas and concepts on TheGlobalMacroTrader.com and associated websites, emails, posts and social media messages constitute valuable intellectual property. No material from any part of TheGlobalMacroTrader.com and associated websites, emails, posts and messages may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of TheGlobalMacroTrader.com. All unauthorized reproduction or other use of material from TheGlobalMacroTrader.com and associated websites, pages and emails shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. The recipient should check any email and any attachments for the presence of viruses. TheGlobalMacroTrader.com accepts no liability for any damage caused by any virus transmitted by this company’s website, emails, attachments, posts and any other method of communication. TheGlobalMacroTrader.com expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. TheGlobalMacroTrader.com reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.