Pre-Fed Meeting Analysis Along with 2024 Scenarios for Stocks and Bonds

Last week was very interesting, even if markets were relatively quiet.

PCE / Income & Spending

PCE, the Fed’s preferred gauge of inflation, came out as expected with now a y/y rate below 3% (even if just below at 2.9%). Looking at PCE with a six-month annualized basis, it is at 1.9% in December below their target.

This is great news, so off to the races? Well, not quite. Other data will concern the Fed.

Also out on Friday was personal income and spending. Income came inline at +0.3% m/m, but spending was hot at +0.7% m/m vs 0.5% expected. GDP for Q4 was also above expectations (more on that below).

The Fed will definitely like the PCE data point. However, they have said that wages are a concern, they remain elevated (jobs data out this week).

Consumer spending rate is also strong. While the Fed could take a victory lap and start cutting, I think given the relatively strong economic performance the Fed is worried about a flare up of inflation again. With no signs of the labor market weakening materially, they have cover to keep pushing on the brakes.

Savings continue to be depleted and credit card usage is increasing. Can consumers really continue to spend at this rate? I think part of the reason for their confidence is that unemployment remains quite low. If more firms start to adjust lower their workforces, which is what I am watching over the first half of 2024, then consumers will also start to pullback.

US GDP

GDP came in at 3.3% q/q seasonally adjusted and annualized, much stronger than the 2.0% expected. This is the advance estimate. (release here)

Services continued to be strong, along with nondurables. Inventory was only a 0.1 of a factor, so no concern about that reversing course next quarter.

While those looking for a soft landing must have cheered, I think many within the Fed did not. Several Fed officials, including Chair Powell, have been stating that the economy does need to slow to ease pressures, especially in the labor market. A growth rate at that level is not conducive to sustained low levels of inflation, especially if the Fed starts to cut. We have to remember that the Fed has an idea of the long-term top speed of the economy and these levels are far above potential GDP. Combine this with wages remaining strong and now shipping costs increasing, 2024 could be a year of headaches for the Fed.

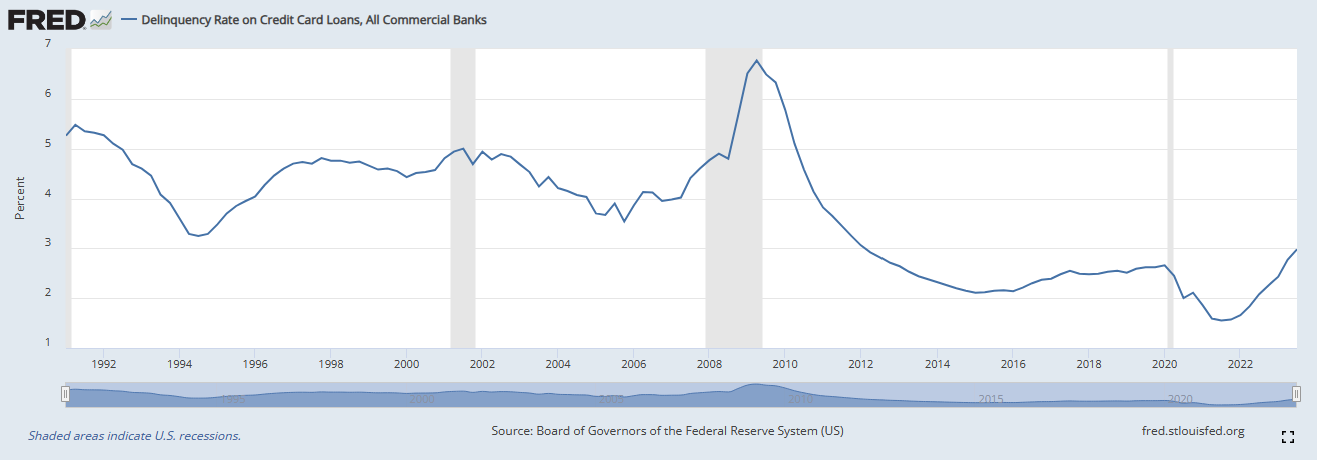

Credit Card Debt

I was curious about the level of credit card delinquencies, from the St. Louis Fed:

We are clearly off the lows. I know that people will say current levels are far lower than the 2008-2009 period, which is true. But trends matter. If the economy is so strong, why are people increasingly becoming delinquent on their credit card debt? Furthermore, will higher rates for longer help or hurt additional delinquencies? (that is a rhetorical question)

The 1994-1995 period is the one that everyone points to as ideal, a nice soft landing. I talk more about that period below. I would caution that we cannot make the comparison as apples-to-apples. Debt levels today are much higher than in the mid 1990s.

I would suggest that additional time at such a restrictive level of monetary policy territory is not conducive to a reversal in delinquencies.

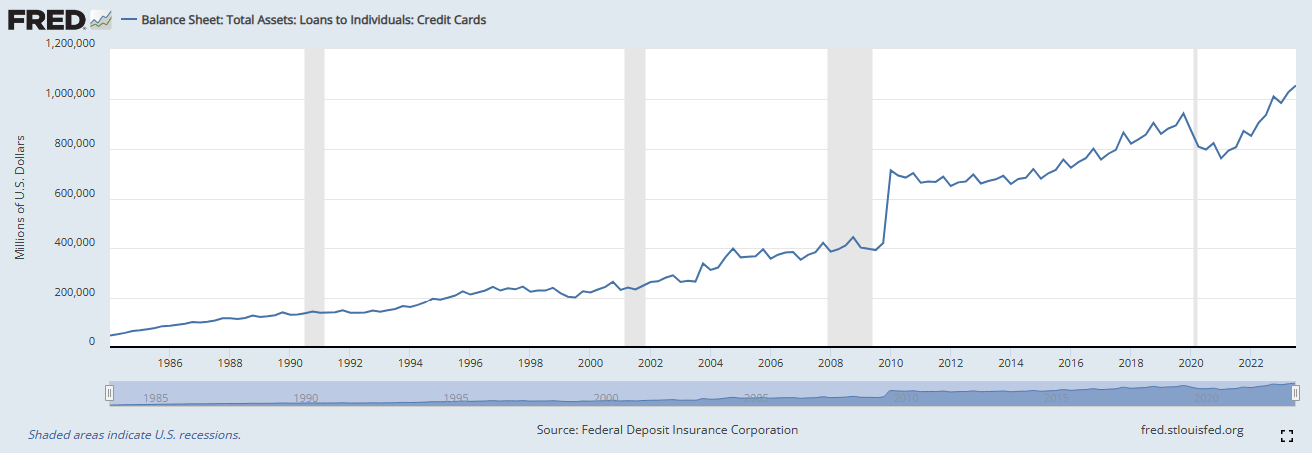

If you did not believe me earlier, this chart includes all credit card loans to individuals. We are far above the levels in the mid 1990s. As long as people have jobs and wages continue to grow at this strong pace, people can afford to pay their bills (at least the majority of people, as some are not able to do so, as noted above). If that changes (ie. more job losses), this situation could escalate quickly. Something to pay attention going forward.

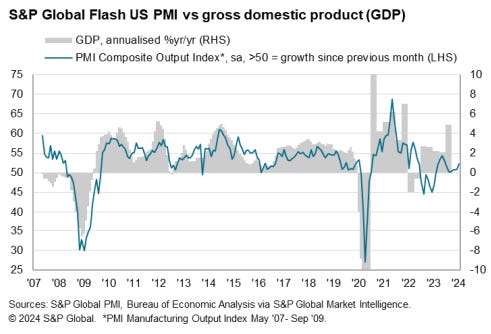

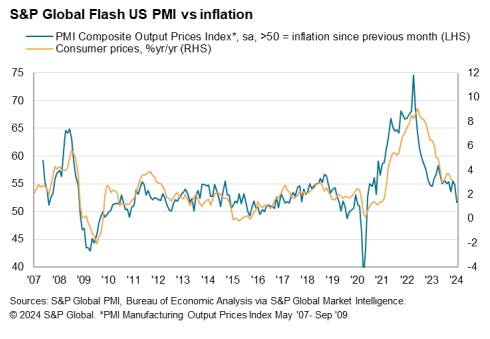

PMI

Global PMI data was out last week. The US (here) came in very strong, with the Composite at 52.3 from 50.9, a 7 month high. Services at 52.9, expanding from the December reading of 51.4 and also a 7 month high. Manufacturing now moved over the key 50 level for operating conditions at 50.3, although output is still contractionary at 48.7.

Excerpts:

“…firms reported stronger new order growth for both goods and services, helping push business confidence for the year ahead to a 20-month high.”

“On the price front, overall input costs rose at a slightly softer pace at the start of the year, while firms raised their selling prices at the slowest rate since May 2020.”

“New business expanded for the third successive month at US companies in January, with the rate of growth quickening to the sharpest since June 2023. The upturn in new orders was broad-based, as manufacturers registered the first rise in new sales since October 2023, and the fastest uptick since May 2022. Service providers reported the strongest gain for seven months.”

“Businesses were more upbeat in their expectations regarding the outlook for output at the start of 2024, as the degree of confidence reached the highest since May 2022.”

Inflationary pressures continue to move out of the system, but the economy looks like it is rebounding. This is a short-term positive backdrop for equities. If inflationary pressures start to reverse, that would be a significant concern for long bonds.

We can go into two directions, the Fed cuts soon and this boosts economic activity or the Fed keeps rates where they are the cracks beginning to form grow worse and economic activity reverses back down. More on various paths below.

Looking Ahead to the Fed Meeting

Taken together, the data indicates that the US economy remains strong. The Atlanta Fed’s Nowcast (here) is estimate Q1 2024 GDP at 3.0%, with the NY Fed Nowcast (here) estimating 2.8% for the same quarter. To be clear, these forecasts are not perfect. However, if a Fed official is looking at this recent data, they would have to be worried about cutting too soon. Especially given how many Fed officials have come out and stated that they do not want to repeat the mistakes of the 1970s, cutting and then being forced to hike once again as inflation flared up. I think the data will give them more than enough cover to not cut in March.

The Fed may signal that QT will be slowing down or even contemplating stopping QT relatively soon. That may appease the doves, as it is one fewer tightening policy. This week Powell may just state that discussions are ongoing. The key issue with QT, banks have to dip into their reserves to provide funding for securities. When the Fed engaged in QE, they bought securities, which injected cash into the system. This cash provided banks the ability to lend or buy other securities, creating a push in economic growth. By definition when one does the opposite, it causes the economy to slow with decreased lending and reduced purchases of securities. There is a limit to how low the Fed’s reserve can drop before it negatively affects the economy.

There is a lot of data over the next few months and it is hard to predict exactly how things will unfold. I am paying close attention (as is the Fed) over labor market conditions. Any sign that the labor market is beginning to slow down and markets will adjust accordingly. That is when I would feel confident in Fed cuts, because if the economy starts to re-accelerate they could not cut unless inflation is firmly in hand, as that would really add fuel to the fire. So far weekly unemployment claims are not signaling a problem and while firms are laying people off, the numbers overall seem relatively low. However, as I noted last week, job postings continue to drop, temporary work is decreasing, let’s see if non-farm payroll data starts to indicate weakness with lower overall job hiring and lower average weekly hours worked.

I think the Fed will keep in language referencing the potential of additional rate hikes if appropriate. If that sentence is removed, they would be signaling cuts are near and markets would move rapidly in that direction. I doubt it, given the strength of the economy, but anything can happen.

Different Types of Cuts

A great question came in last week asking about my views if the next Fed cutting cycle will be different than the others, in that last week I talked about the Fed most likely pushing out the first cut beyond March. I should clarify both my short and long term view.

Several Fed officials have tried to convey the message that the next rate cutting cycle will be different than the recent past, which were as a result of economic weakness. Those rate cutting cycles were quick and large in magnitude. Currently the Fed is trying to signal that the Fed wants to get back to “fine tuning” monetary policy, as it had in the past.

There have been many instances that the Fed would ease slightly to “fine tune” monetary policy but not cut all the way to the floor. This includes the cuts on November 6th 2002 for 50bps and June 25, 2003 for 25bps. This was a couple of years post dot.com bust and the economy was still weak and inflation falling deeper below the 2% target.

The three 25bps cuts in 1998 were out of concern related to the Asian currency crisis (plenty of info on that online).

The 1994-1995 period is what most are hoping for in terms out outcomes. The Fed started raising rates in February 1994 and completed their hikes one year later, a total of 300bps higher in the Fed funds rate. Following the recession that started in 1990, the Fed cut rates with the last one being September 1992. It was a couple of years of slow recovery, before a strong GDP growth figure of 4% in 1993. Worried that growth may accelerate leading to higher inflation, Greenspan’s Fed raised rates starting in 1994. The economy started to slow somewhat in 1995 and the Fed reacted by cutting rates three times by 25bps each. The soft landing was achieved and the economy grew strongly from the mid 1990s-2000.

Given the current strength of the economy, the Fed does not believe that a crisis is imminent and as such thinks that some fine tuning is all that is required. It does not matter what I think, if they are right or wrong, but rather their view is what counts.

As I will not fight the Fed, I will continue to lean on the side that cuts are not coming soon. Yes, the Fed will cut, but given the number of comments related to concerns over inflation flaring up again, combined with the recent retail sales data (better than expected), spending data (better than expected), PMI data (better than expected), GDP data (better than expected) and so on, they will most likely take the cautious approach. As I have discussed before, with the unemployment rate so low, they do have some cover to keep such high restrictive monetary policy in place.

My concern is that historically when monetary policy is this restrictive, a recession usually occurs. The longer they keep rates this elevated, the higher the probability of a recession.

However, if there is no recession soon and they do start cutting, then one has to move quickly to the other side of the boat. Given the number of data points that are beating expectations and coming in strong, Fed cuts over the short-term before signs of a contraction will add fuel to the economy. I would go long equities and short fixed income at that point.

If the economy starts to crack, it is at that point that I think Fed cuts will be greater than the market expects.

If the economy holds steady, the Fed may continue to push out cuts further out in 2024.

The market expects 125-150bps cuts for this year. The Fed believes the neutral rate to be in the range of 250bps, far below current levels. If the economy really does slow (still to be determined), then I find it hard to believe that the Fed would not at least move down to or even perhaps slightly below neutral. It would be hard (in my opinion) to justify holding rates in restrictive territory if signs of economic slowing were to be present.

The data will drive the actions. Either

The Fed will leave rates at current levels for longer than markets expect, and most likely fewer cuts than 125-150bps (if the economy continues to surprise to the upside), or

The Fed will be forced to cuts by more than the market expects and I suspect at a quick pace if the economy slows down and indicates a possible recession.

If there were to be an economic slowdown, I think it most likely would be a mild one. The fundamentals appear solid. It would be a great entry point for equities following a sell-off, with the Fed cutting and pulling the economy out of a recession with a strong 2025-2026.

Naturally, if there were an area of the economy that would implode and create stress throughout the entire system that is quite different, but I do not see the same 2008-2009 build-up in one sector that could lead to a severe crash - it could happen, but hard to foresee at the moment. The new “hot” sector over the past decade has been private credit. Perhaps that is the area of concern, but hard to know ahead of time.

Economic Paths in 2024

The path this year could be for the economy to show signs of a slowdown in the first half of 2024, the Fed sees these signs and starts to cut aggressively. Under this type of scenario, the economy and equities could rebound quite strongly by 2025. There would be an initial pullback in equities and yields would drop, but as the Fed embarks on cuts the weakness in equities would be a buying opportunity.

Conversely, the economy could keep moving along relatively strongly, the Fed achieving its target of 2% starts to cut, this would be equity bullish and bond bearish (longer duration). The economy would get a positive jolt of energy, margins can expand again, and those interest rate sensitive sectors would benefit in addition to long duration assets (ie. tech stocks). I think longer duration bonds would sell off and yields climb, as worries over inflation would be stoked - not initially, but as the economy gains even more steam worries would emerge.

Those are just two paths, there are several more, but these are two on either side of the continuum of potential outcomes.

Earnings Season

Earnings season continues. This week plenty of big names will be out. So far about 25% of S&P 500 companies have reported. Companies are reporting negative Q4 2023 earnings. Recall last year most analysts were thinking that earnings growth be close to double digits positive, which I thought hard to believe at the time - this positivity has all been pushed out into 2024.

The forward P/E is now 20, this is not cheap territory, far above the 10 year average of 17.6. Any misstep by a company and they will be hit hard (for example Intel).

Still too early in earnings season, but the next couple of weeks will be interesting and possibly set the tone for equities over the next little while.

I think one of the main concerns will be a) if there is a recession, which analysts are not pricing in, how much of a decline in earnings will we see, and b) will margins expand this year. These are somewhat related, but both important to consider.

Profit margins are still near all-time peak levels. Can they continue to expand with finance costs increasing, along with wages? I think it is a hard case to make, especially given that as inflationary pressures recede, which will help firms on the input side, they will have trouble raising prices to consumers.

Regarding a recession, even if it is a mild one with earnings declining 5-10%, which is not extreme at all, and multiple pullback within the 5-10 year forward P/E averages of 17-19, leads to an S&P 500 in the range of 3700-4100 (all approximates).

The important point to consider, since very few think a recession will occur, the market is leaning very heavily on the other side of the boat - the biggest moves occur when markets shift from one side to the other. Any sign of an economic slowdown and I fully expect a very sharp sell-off in equities. Not yet, but I am watching closely. For long-term investors, this would be a good time to perhaps add some hedges, such as buying put options (ie. bearish strategies) or selling covered calls and so forth.

What to Watch This Week

The Fed on Wednesday, already discussed

Jobs data on Friday. Expectations are for 177k, with the unemployment rate to tick higher at 3.8% and avg hourly earnings to tick lower at 0.3% m/m.

There have been few misses vs expectations recently. I count November and August of last year missing expectations, and then one needs to go back to April 2022 for the next prior miss.

Conversely, going into the negative print in February 2008, 6 of the 12 months going into that print had actual numbers miss below expectations.

Let’s see if expectations continue to be met, or the data starts to disappoint.

JOLTS data is out on Tuesday

The data continues to show lower job openings, which is contrary to other data discussed earlier (PMI, GDP etc…). Will have to see how this all works itself out. Job openings are an early warning sign that the economy is starting to lose some steam. There could be pandemic considerations, perhaps there were too many postings following the pandemic, but I will still be concerned and watching this area closely.

ADP is out on Wednesday. Not many people use this data set, but still interesting to review.

Equities

I still hold a position in the S&P 500 (this is the SPX index) from 4400 area (see prior weeks for more info). I am moving my stops further higher in the 4830-4840 area.

This will not be that profound at all but stating the obvious when I say that we are at an important point for equities. The move higher from October has been very strong, but momentum is now fading. It seems that regardless of what indicator you use, (in this case MACD, RSI, CCI) they are all showing that momentum is slowing. The market was also in a tight range last week. Obviously investors are waiting for earnings season, the Fed and data to help guide their next moves.

The S&P 500 can either breakout higher through this recent top, or break down. If the S&P 500 starts to crack lower, other traders who are more technically focused will point to negative divergence and other indicators of weakness, creating overhead supply through selling pressure. I would not go short yet but close my long, wait and watch closely for a good risk:reward entry point. A move higher would add some momentum into the rally for a further move higher.

I cannot predict what will happen, but given at how expensive stocks are currently and priced for perfection, I just know that perfection rarely occurs (sometimes, but I would not bet my life on it). I think we might be close to a top. Is it a short-term consolidation or start of something bigger? Hard to know at this point. I will let the market action help inform my decision.

Fixed Income

This is the 10 year yield. The next few days yields may drift higher, as the next schedule US Treasury refunding announcement will be this week. I think that unless the announcement comes out with a significant surprise higher, the markets have already priced in elevated issuance levels. On the other side (buyers of fixed income assets), I have talked with some PMs that are looking to buy on pullbacks. These are long-term real money managers who are happy to see inflation continue to drift lower. This decreases their concerns over long-term inflation and are happy to add duration on pullbacks. Could we see higher yields, yes of course. But I don’t think we will see 5%, as inflation continues to decline. I can see a backup towards 4.25%, which looks very attractive as inflation heads towards 2% (or below, as PCE is with a six-month annualized basis). If that trend continues, I think we will see at least 3.50% at some point this year. I continue to look at trading ranges in the 10 year, buying in the 4.10-4.20% and looking to trim around 3.80%. I think there will be a few oscillations back and forth this year.

If the Fed cuts sooner rather than later and the economy is showing this level of strength, I would close my 10 year long and re-evaluate as that would stoke inflationary fears.

As discussed earlier, if the economy does indicate signs of weakness, I would aggressively move towards the front of the curve as the Fed will (in my opinion) cut by more than the market thinks, moving towards (or even through) their neutral level of 2.5%. The 2 year would drop sharply in yield.

Oil

Oil has now begun to look interesting. It has moved up quite a bit and I don’t like to chase the market, so I will wait and see if it consolidates. If it does, I will look to put on a long, but if it continues and I miss the move, so be it. I will discuss this more next week if it still looks interesting.

Gold

I did put on a small short position and closed it out at essentially flat. Gold does not look like it wants to move lower. Also notice the descending line, a move higher could result in additional buyers stepping into the market.

It is strange because as the US economy is showing strength, this should be positive for the US dollar and a headwind for gold. However, gold appears to be getting ready to move higher. Too many cross currents and I will stay on the sidelines for now.

Thanks for reading!

theglobalmacrotrader@gmail.com

Twitter —> @TheGlobalMacro

Disclaimer

Copyright (c) TheGlobalMacroTrader.com 2024. All rights reserved. All material presented either through the TheGlobalMacroTrader.com website, Substack, any newsletter published by this site, posts on any social media platform and other public comments are not to be regarded as investment advice, but for general informational and entertainment purposes only. You, the reader, assume the entire cost and risk of any trading you choose to undertake. You, the reader, are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice and are for entertainment purposes only, no advice has been presented and no recommendation have been made. All information on TheGlobalMacroTrader.com, and any associated pages such as the SubStack pages, are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings along with discussion over chart formations and quantitative metrics may be mentioned but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security—including commodities, currencies, stocks, bonds, exchange traded funds (ETF), exchange traded notes (ETN), mutual funds, futures contracts, or any similar instruments. All text, images, ideas and concepts on TheGlobalMacroTrader.com and associated websites, emails, posts and social media messages constitute valuable intellectual property. No material from any part of TheGlobalMacroTrader.com and associated websites, emails, posts and messages may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of TheGlobalMacroTrader.com. All unauthorized reproduction or other use of material from TheGlobalMacroTrader.com and associated websites, pages and emails shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. The recipient should check any email and any attachments for the presence of viruses. TheGlobalMacroTrader.com accepts no liability for any damage caused by any virus transmitted by this company’s website, emails, attachments, posts and any other method of communication. TheGlobalMacroTrader.com expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. TheGlobalMacroTrader.com reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.