Why I Am Holding onto my Stock Short Position. Also, Reasons to Worry About the Consumer even as Retail Sales Were Strong Last Month.

Why I Am Holding onto my Stock Short Position. Also, Reasons to Worry About the Consumer even as Retail Sales Were Strong Last Month.

** Please note that I will take some time off and not publish a report for a weeks.

Retail sales came out stronger than expected, all is clear? Not so fast.

Yes, we all know that retail sales came in at 0.7% m/m vs forecast of 0.4%, with core at 1.0% m/m vs 0.4% forecast. However, we should not be surprised to see the consumer holding in for a little longer.

Here are a few considerations.

Many home owners locked in long-term mortgages, higher interest rates are not affecting these folks to the same degree (yes, there are higher rates in other areas, but mortgage payments are a large capital outflow for households)

Savings were high post-pandemic, albeit they are being drawn down. More on this below.

Employment remains resilient. I have talked before that the unemployment rate is not a leading indicator, it tells us where the economy is today and was yesterday, not where it is going tomorrow/next month/quarter.

All of this is to say that just because the consumer has some additional cash to spend last month (either savings or debt) it is not an “all clear sign”.

There was an interesting and excellent follow-on update by the San Francisco Fed (located here) of an earlier paper, “The Rise and Fall of Pandemic Excess Savings” (that one is located here). In the report, they reviewed household saving patterns since the covid-19 recession.

Excerpts:

Our study showed that households rapidly accumulated unprecedented levels of excess savings—defined as the difference between actual savings and the pre-recession trend—relative to previous recessions. Our analysis suggested that some $500 billion of the $2.1 trillion in total accumulated excess savings remained in the aggregate economy by March 2023.

Since then, data revisions show noticeable changes in household disposable income and consumption, while new data releases indicate that consumer spending picked up in the second quarter. Our updated estimates suggest that households held less than $190 billion of aggregate excess savings by June. There is considerable uncertainty in the outlook, but we estimate that these excess savings are likely to be depleted during the third quarter of 2023.

We are in the third quarter currently, with expectations that excess savings are to be completed depleted. This is yet another headwind for markets. Savings are being drawdown, consumer debt load is increasing, student loans will have to start being repaid and the level of real interest rates is increasing as inflation subsides.

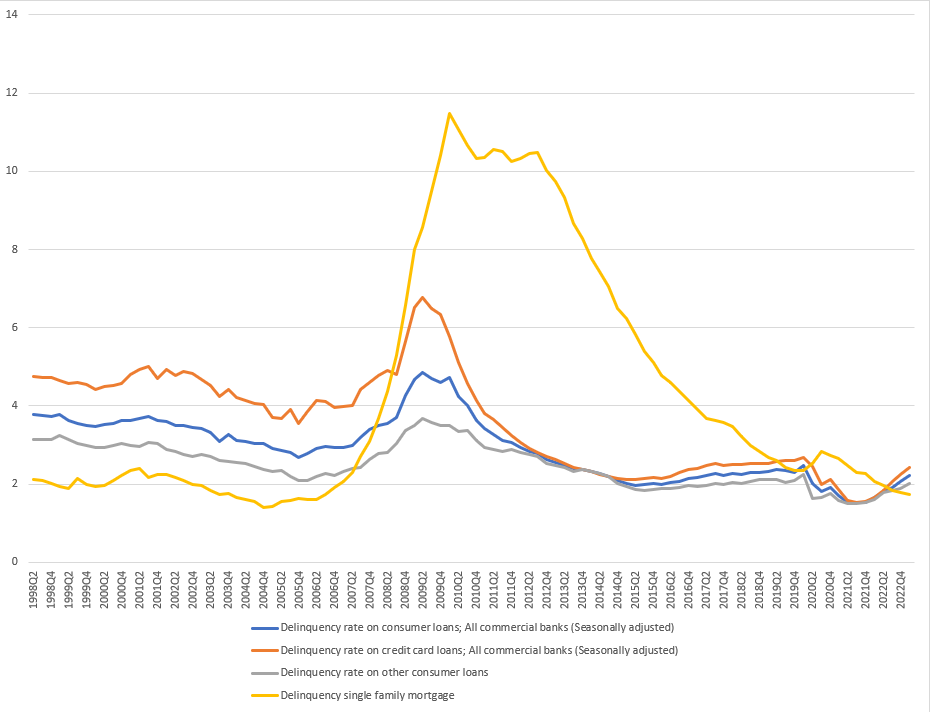

This chart was built using data from the Federal Reserve (located here) with a subset of data, specifically looking at delinquency rates. I was curious over the past few decades, where are delinquency rates for consumers today versus the past?

The yellow line is for family mortgages. As I noted earlier, many homeowners locked in long-term mortgages - as long as they have a job, they will pay their mortgage, theoretically. The data supports this theory, as delinquency rates have remained very low.

The other three lines are more interesting, delinquency rates on credit cards (orange), all other consumer loans (grey) and all consumer loans (blue), with the data comprising of all commercial banks and seasonally adjusted.

All of these areas (non mortgages) have recently experienced a rise in delinquencies. I think this is important to consider, especially given all of the other headwinds. Retailers have already started indicating their worry going into the next few quarters.

It is true that the absolute level of delinquencies remains low, but the move higher in percentage terms is surprising. If the economy is so strong, what is driving this move higher in delinquencies? Monetary policy must be the primary contributor, as we cannot point to massive job losses.

Also note that in during the 2008/09 period, we saw credit card, and other debt, delinquencies break higher in Q4 2007, before really accelerating in late 2008 and 2009. In early 2001 consumer delinquencies on credit cards also increased. This is an area I am watching, people tend not to become delinquent on their debt unless they have to, for one reason of another.

Is this the a guarantee of economic stress? Of course no one knows the future, but when combined with ever higher real interest rates (as inflation decreases and interest rates remain the same or higher, this increases real interest rates) and longer than normal restrictive monetary policy stance, the odds are stacked against the consumer, who drives the U.S. economy.

Consumer Focused Company Results

We have had a number of retailers come out with earnings. On the whole, not bad. However, I think there are some signs of concern going into the end of 2023 and into 2024. Some thoughts:

Target comparable sales dropped 5.4%, as discretionary spending declined. They reported being very cautious in their outlook for the rest of 2023. Target has less focus on groceries, unlike Walmart, so their revenue fluctuates more often based on discretionary spend. They have issues of their own to deal with, such as inventory excess that they are working through. The CFO is preparing for more headwinds with the statement, “Student-loan payments will cause additional pressure on already strained consumer budgets.”

Home Depot, comparable sales declined 2%, although better than expected. The types of products purchased will be interesting to note, how many are large durables (ie. washing machines) versus small upgrades (ie. paint). Interesting that total customer transactions fell, while average ticket price increased. This is as a result of inflationary pressures helping overall revenue, not as a result of increasing number of sales (units). Don’t forget, new home demand is still strong, we should see this help a firm like Home Depot, yet they noted softness in larger-ticket items such as appliances.

Walmart, comparable sales were strong at +6.4%, slightly lower than last year’s numbers but better than forecast. A large portion of Walmart sales are groceries. I want to discount those, as they are not really optional. Sales did fall in home goods and sporting equipment. The thing to note, Walmart is the low cost leader. During an economic downturn, people will go to Walmart in order to maximize spending, as noted by the increase in shoppers making over $100,000 since the pandemic, but seeing some of the non-grocery areas weaken is one area I will focus on going forward.

A non-US retailer, Canadian Tire also is indicating areas of concern. The CEO stated, “With 10 interest rate hikes in less than 18 months and persistent inflation impacting the cost of living and leading to reduced savings cushions, Canadian consumers are experiencing increased financial strain and facing tougher spending decisions.” The firm’s own internal analysis indicates that debt-burdened consumers are pulling back spending on discretionary goods.

Yes, there are some different in Canada, but is the US consumer that different? I keep asking myself, can the consumer be able to withstand so many headwinds? (savings eroding, higher rates, repayment of student loans, tighter banking credit conditions etc…) I would not take that bet.

One more comment on the consumer from former Bank of Canada Governor Stephen Poloz in an interview, “I don’t think the consumer is as resilient as the data will make them look.” He believes it is just a matter of timing before tighter monetary policy bites into the economy. He also noted that the low unemployment rate should not be viewed completely from the lens of economic strength. Poloz thinks that changes to the labor force, with a substantial amount of workers retiring, is helping keep the unemployment level low. This may result in monetary policy remaining too tight for too long.

Fed Minutes

The minutes from the last Fed meeting were released (located here). I noted this during the last publication of Fed staff’s economic forecast, they are trying to thread the needle and prevent markets from anticipating a Fed cut over the near-term, but keeping that option open longer-term by saying:

“The economic forecast prepared by the staff for the July FOMC meeting was stronger than the June projection. Since the emergence of stress in the banking sector in mid-March, indicators of spending and real activity had come in stronger than anticipated; as a result, the staff no longer judged that the economy would enter a mild recession toward the end of the year. However, the staff continued to expect that real GDP growth in 2024 and 2025 would run below their estimate of potential output growth, leading to a small increase in the unemployment rate relative to its current level.”

This is to be translated into, “markets - do not price in cuts yet, push that out into late 2024 or 2025”. Something I have been trying to get across for months. However, their model is at odds with street economists. Most economists are forecasting the economy to accelerate into the end of 2024 and into 2025. Both groups cannot be correct!

Some inflation related statements:

“Risks to the staff’s baseline inflation forecast were seen as skewed to the upside, given the possibility that inflation dynamics would prove to be more persistent than expected or that further adverse shocks to supply conditions might occur.”

“Participants assessed that the ongoing tightening of credit conditions in the banking sector, as evidenced in the most recent surveys of banks, also would likely weigh on economic activity in coming quarters. Participants noted the recent reduction in total and core inflation rates. However, they stressed that inflation remained unacceptably high and that further evidence would be required for them to be confident that inflation was clearly on the path towards the Committee’s 2 percent objective.”

Things are moving in the right direction, but they are not yet convinced. This means, the risk to the economy is to the downside. They are looking in the mirror (backward data) to drive the car (what will happen in the economy tomorrow/next quarter). The Fed is so concerned about inflation that they are willing to look past current evidence of a slowing economy, such as “ongoing tightening of credit conditions”. I think the lag effects have yet to fully take hold of the economy, which could result in a quicker downturn than they have forecasted.

I think what is interesting to note was that there were members who are worried about downside risks to the economy, but Powell has been focused on communicating the upside risks to inflation.

“In discussing downside risks to economic activity and inflation, participants considered the possibility that the cumulative tightening of monetary policy could lead to a sharper slowdown in the economy than expected, as well as the possibility that the effects of the tightening of bank credit conditions could prove more substantial than anticipated.”

I think Powell is trying to ensure the narrative is one of an inflation-fighting Fed. This is a smart move, as markets were pushing for Fed cuts in this month earlier in 2023. I think Powell will keep at this hawkish narrative until signs are clear that inflation is approaching their target. If not, markets will front-run Fed cuts and jeopardize the Fed’s work, or create even more work for the Fed (ie. more Fed hikes to combat easing at the longer-end).

Jackson Hole

The theme this year is “Structural Shifts in the Global Economy.” The indication to me is that they will be talking about monetary policy in a post-pandemic world. Has the monetary policy transmission shifted since the pandemic? That may be one of the questions discussed. They may also discuss what is a restrictive level of monetary policy in the current economic situation.

In terms of current Fed policy, I would fully expect that Powell will re-iterate that inflation is far from target and they are concerned about upside risks. I cannot see why he would deviate from that message. If anything, one takeaway may be that the Fed is considering that economic shifts have resulted in the need for an even higher level of terminal. That should continue to provide selling pressure for fixed income and elevate yields. But it is very hard to predict these events. Much better to listen and interpret what has been stated.

Equities

As I wrote in the last report, I initiated a short position in the S&P 500 just above the 4500 region. I did close a little of the position to take profits on Friday and will continue to do so around current levels, as I think the 4325-4335 area might be one of support. If the S&P breaks through these levels, I would expect the next area of support will be in the 4200 region, as the 200 day moving average meets this prior area of support/resistance.

I always hold some portion for an even larger move (ie. beyond any target I may set) of course, with a market reversal as a way to stop my positions out (trailing down). My current stop will be moved down towards the 4500 region, or around breakeven essentially. Another “free” trade (although I hate to use that term, as my goal is to squeeze out as much profit as possible, not to move stops to just breakeven, but it is easy to conceptualize).

A former colleague asked me last week if the move down was not sufficiently fast enough to take profits? I said that to a degree yes, but only partial profits (as described above). First, the move down is not what I would consider a panic. One easy way to see that is by using a momentum oscillator such as the CCI (bottom panel). Typically when the CCI (there are various periods, just be consistent) moves below -200 it is a sign of possible short-term capitulation. We are not there yet. What I would expect as possible is a consolidation of this move down, with the S&P 500 oscillating perhaps even up to 4400ish area, then another move down breaking below the current lows. That would be a nice set-up for a move towards 4200. If I am wrong, it will re-accelerate up towards and through 4500. Given my concerns noted above, that would be a headscratcher of a move. Note there is a bearish divergence between the S&P 500 and both the MACD and RSI. Again, not a “magic” technical development, just a sign that the recent move up was accompanied with lower levels of momentum. I like those types of developments in addition to fundamental drivers.

Fixed Income

This is a substantial move in the long end (10 year, but 30 year is similar). We are potentially about to breakout out of very key levels. These are technical moves. Yes, the Fitch downgrade was a factor, but I would suggest a minor one. Rather, I think the markets are trying to adjust with the increased level of supply coming down the pipe. So far the long-end does not believe there is substantial economic weakness coming. That is a possible opportunity to enter this type of trade, but not yet. Let the technicals push yields higher before the fundamentals kick into gear over the next few months.

This is the 10 year Japanese Government Bond yield. Also note that the adjustment in yield curve control by the Bank of Japan to permit 10 year yields to move up 1% may also be a factor of having net dispositions of long-term debt securities according to the Japanese Ministry of Finance. We would normally expect buyers from Japan, this is not currently the case (some variation between weeks).

Overall, I am still sitting on the sidelines. For the front-end of the curve, I need to see some deterioration in the economy to give me an idea of when the Fed will cut (nowhere in sight just yet). However, the long-end of the curve will start to look attractive to myself and other investors if we can get a little higher in yield, reach some old levels not seen in over a decade, such as 5.50% (not a standing buy order, rather an area that I would evaluate buying, depends on how we got there and so forth).

Oil/WTI

This is the weekly chart of WTI (continuous contract, note that prices are slightly different between the front months, direction is similar however).

I went long in the $74 region, as I wrote late time “I am looking at this $83ish region for a partial profit taking zone. Having said that, if WTI is able to get through that area of resistance, it has a decent probability of moving into the low $90s range. There should be sellers/resistance around $83ish region…”

In the continuous contract chart, price did exceed the $83ish area nicely, and I took some profits. Frankly, given the news out of China, how their economy is weakening, oil should have sold off more than it did (in my opinion). Being able to stick around in this region is interesting, and supports holding the remainder of my position. Friday was a nice day, as WTI is trying to regain the lost ground.

Will WTI definitely move higher? I have no idea, but there are both fundamental and technical drivers that are bullish. Even so, if the market breaks down through the $77.50ish range, I would close the position (again, with partial profits out already and entry around $74, it is now a risk-free trade).

The chart above I have shown a few other times when WTI was above the 50 week moving average and the market stalled. In some cases it continuing moving higher, in others it pulled back further. Knowing that I will be wrong a lot of the time (as are all traders), this is why I ensure that my risk/reward setup is as attractive as possible, including having as many positive tailwinds (ie. fundamental, technical).

The market may consolidate here and I am willing to wait and see how things turn out. The next target area would be about $10 higher, in the $93-$94ish region.

Gold

This is the weekly chart of gold.

Patience, or lack thereof, was my Achilles heel for a long time. Knowing one’s blind spot(s) is important part of becoming a better trader and investor. While I thought gold may have been setting up for a breakout, the technicals just were not there for a trade, so I sat back and waited. As I wrote in the last report, “I still do not see a compelling risk/reward set-up. I don’t care how strongly my own beliefs are about an asset and potential trade, if I do not see an above average risk/reward set-up, I will not enter the trade. We may very well see gold trade side-ways for a little while, perhaps drop down further or it may break upwards through this recent top at $2010ish. I will wait and see.”

I look through the lens of breaking every trading possibility into risk/reward, and this has been crucial to ensuring that I am able to fight another day. This recent period in gold was a great example of no trade, resulting in avoidance of loss. (with the S&P being a positive example). There were signs that gold was getting ready to breakout, yet I could not pull the trigger based on lackluster risk/reward.

So where are we know?

Given the increase in yields (and real yields), and increase in the dollar, combined with unfavorable risk/reward, I have to remain on the sidelines for longer. I would be leaning short, but if I were to do so around 1916, with a stop in the 2000 area, I would need to be confident that gold would break down below 1700 - this is not something that I have high confidence of occurring. As you can see on the chart, between the 50 & 200 week moving averages, along with several areas of probable support, it will be a tough move down. As such, I will continue to wait and see.

Thanks for reading!

theglobalmacrotrader@gmail.com

Twitter —> @TheGlobalMacro

Disclaimer

Copyright (c) TheGlobalMacroTrader.com 2023. All rights reserved. All material presented either through the TheGlobalMacroTrader.com website, Substack, any newsletter published by this site, posts on any social media platform and other public comments are not to be regarded as investment advice, but for general informational and entertainment purposes only. You, the reader, assume the entire cost and risk of any trading you choose to undertake. You, the reader, are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice and are for entertainment purposes only, no advice has been presented and no recommendation have been made. All information on TheGlobalMacroTrader.com, and any associated pages such as the SubStack pages, are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings along with discussion over chart formations and quantitative metrics may be mentioned but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security—including commodities, currencies, stocks, bonds, exchange traded funds (ETF), exchange traded notes (ETN), mutual funds, futures contracts, or any similar instruments. All text, images, ideas and concepts on TheGlobalMacroTrader.com and associated websites, emails, posts and social media messages constitute valuable intellectual property. No material from any part of TheGlobalMacroTrader.com and associated websites, emails, posts and messages may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of TheGlobalMacroTrader.com. All unauthorized reproduction or other use of material from TheGlobalMacroTrader.com and associated websites, pages and emails shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. The recipient should check any email and any attachments for the presence of viruses. TheGlobalMacroTrader.com accepts no liability for any damage caused by any virus transmitted by this company’s website, emails, attachments, posts and any other method of communication. TheGlobalMacroTrader.com expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. TheGlobalMacroTrader.com reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.