If March Fed Cuts are Off the Table, Now What Happens?

If March Fed Cuts are Off the Table, Now What Happens?

Unless something material changes, March Fed cuts are off the table (for now).

Jobs

What can I say about the jobs data that has not been said? It was strong, across the board. There are some seasonal adjustments in the recent report, which need to be taken into account, but overall one cannot completely discount this strong print.

Excerpts from the report (located here):

In January, job gains occurred in professional and business services, health care, retail trade, and social assistance.

Services remain a strong area of growth.

Employment in temporary help services changed little over the month (+4,000) but is down by 408,000 since reaching a peak in March 2022.

Temporary help while slightly positive, has been in a downtrend over the past year. An early indication that businesses are full with resources and do not require additional temporary help.

Wages are a concern that the Fed will continue to focus on given the possibility of a even further increases in wages, especially in the services sector. Average hourly earnings increased 0.6%, a very hot number.

The unemployment rate remains stable. The labor force participation rate was unchanged. Hours worked dropped, but that is most likely due to weather.

The revisions to the prior months are getting a lot of headlines. I can understand that, as it puts a new light into the actual level of economic strength. One thing to consider is, as everyone knows, December is a holiday season month and the majority of revisions were to that period of time. November was revised up by 9,000 to +182k while December was revised higher by a very large 117k to +333k.

The real question is what happens in Q1 and Q2 of this year, as I have stated before, since that will help drive business plans for the remainder of the year.

While I understand the narrative that this time is different given the pandemic level of fiscal and monetary stimulus that has led to excess savings, along with stronger than expected Q3 & Q4 2023 growth, I would also suggest that things can shift quickly. Pointing to just the prior quarter of growth as “proof” that the next year will also be strong is not sufficient. I can point to many other reasons for optimism, but it takes more than one or two of strong GDP data points.

As an example, in 1999 GDP accelerated throughout the year before creating a volatile top in 2000 and dropping in 2001. These are the percentage GDP changes from the preceding period:

1999 Q1 3.8%

1999 Q2 3.4%

1999 Q3 5.4%

1999 Q4 6.7%

2000 Q1 1.5%

2000 Q2 7.5%

2000 Q3 0.4%

2000 Q4 2.4%

2001 Q1 -1.3%

In 2007, the year also started to get traction and positive momentum from 2006:

2007 Q1 1.2%

2007 Q2 2.5%

2007 Q3 2.3%

2007 Q4 2.5%

2008 Q1 -1.7%

We all know how 2008 ended, with a dismal -8.5% decrease in Q4.

As I stated before, I do not think that the economy will experience a 2008-like year, but I am cautious that some slowdown is still quite possible given the duration of restrictive monetary policy.

One final comment on the jobs report, having a strong January print is not unusual. For example:

December 2022 print was +223k vs 200k expected followed by a January 2023 print +517k vs 193k expected (Q1 2023 was positive GDP at +2.2% q/q but lower than Q4 2022 of 2.6%)

December 2021 print was +199k vs 426k expected followed by a January 2022 print +467k vs 110k expected (Q1 2022 was negative GDP, coming in at -2.0%)

Just because January is a strong print does not necessarily result in a strong quarter, let alone a strong year.

FOMC

Powell was quite clear, even before the jobs data, unless the Fed was to receive information indicating that the path seen so far on inflation/jobs/economy shifts significantly, March cuts are not on the table.

This clearly supports the view I have been advocating for sometime, the markets were far too aggressive in pricing Fed cuts this year.

The FOMC statement removed the statement “any additional policy firming”, and included “The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.”

This sentence further supports the notion that March cuts are highly unlikely, even before Powell had the press conference. Powell did re-iterate that a few data points are not enough, I believe the Fed needs to see a much large sample size to ensure that inflation truly has been killed.

The statement by Powell that, “There was no discussion on cutting rates. We are not a that stage.” was also important indicator that March is off the table as the Fed usually signals upcoming changes by starting the discussion first within the meeting prior to enacting changes (unless there is need for emergency actions).

Powell also discussed that lower goods inflation will at some point flatten out, at that point the disinflation will have to come from the services side. This statement also indicates that taking the PCE data is not enough, they are looking at the components, and specifically services. In that case, when we see positive inflation data, yet services are not contributing to the disinflation story, and if markets run hard to push for cuts - this may create trading opportunities to fade those moves.

Bottom line, the Fed needs to see services disinflation before cuts begin unless the labor market weakens materially. Powell was quite clear on that latter point, with the statement, “If we saw an unexpected weakening in the labor market that would certainly weigh in favor of cutting sooner.”

What Am I Worried About?

I have been writing for sometime that while most believe in the soft landing scenario, I think given historical events and the level of restrictive monetary policy that a recession is still a reasonably elevated probability this year.

I have been careful not to trade this view, as I stated that the data needs to confirm this thesis. As such, I have not been short equities (in fact long) and avoided being long the 2 year other than short periods of time for a trade (see prior reports).

However, I am slightly more worried after the jobs report about the possibility of a much stronger economy. I do have a 10 year position on because I think inflation is coming towards target and there appears to be limited data indicating that prices will flare up. Also given the duration that monetary policy will remain restrictive, this increases the probability of an economic slowdown.

What if the economy re-accelerates and the Fed cuts? As I wrote last week, I would get out of any fixed income assets (in fact most likely go short) and go very long equities, as this would result in a massive rally in equities until the Fed started to announce they are about to hike rates again.

It is still too early to call it, but I am watching and, as always, worried about what I may be missing.

Treasury Auction Announcement & Participation

One concern I had going into last week was the announcement over Treasury auctions. As I stated, yields may move higher if there was an increase above expectations. However, that did not happen and the Treasury announcement was inline with expectations.

One interesting item from the recent auctions is that participation from investment funds has increased as they take down a greater share of auctions. Funds are much more price sensitive and indicative of where they are interested in participating and therefore gives me an idea (however rough) of yields they are interested in going forward.

AAII Bull Bear Sentiment

The latest AAII sentiment report clearly indicates that retail investors have turned bullish, with the title “Optimism Skyrockets While Neutral Sentiment Decreases” (report located here).

Bullish sentiment increased to 49.1%, up 9.8 points, which is categorized as unusually high. Setting aside the high number in December, if we look back at prior periods when AAII bullish sentiment was at or near 50%, these included:

July 20, 2023 51.36%

November 11, 2021 48.00%

July 1, 2021 48.65%

March 11, 2021-April 22, 2021 all above 48.94% (peak 56.91% April 8, 2021)

December 3, 2020 49.07%

December 14-December 28, 2017 all above 50.50% (peak Dec 28 at 52.65%)

November 24, 2016 49.89%

I know some people like to assume that retail investors are always wrong, but that is not the case. In just these examples, admitting that the sample size is small, looking at how the S&P 500 performed over the next several weeks/months, the last 2 were near interim peaks, one period was essentially a flat and the other four periods the market continued higher.

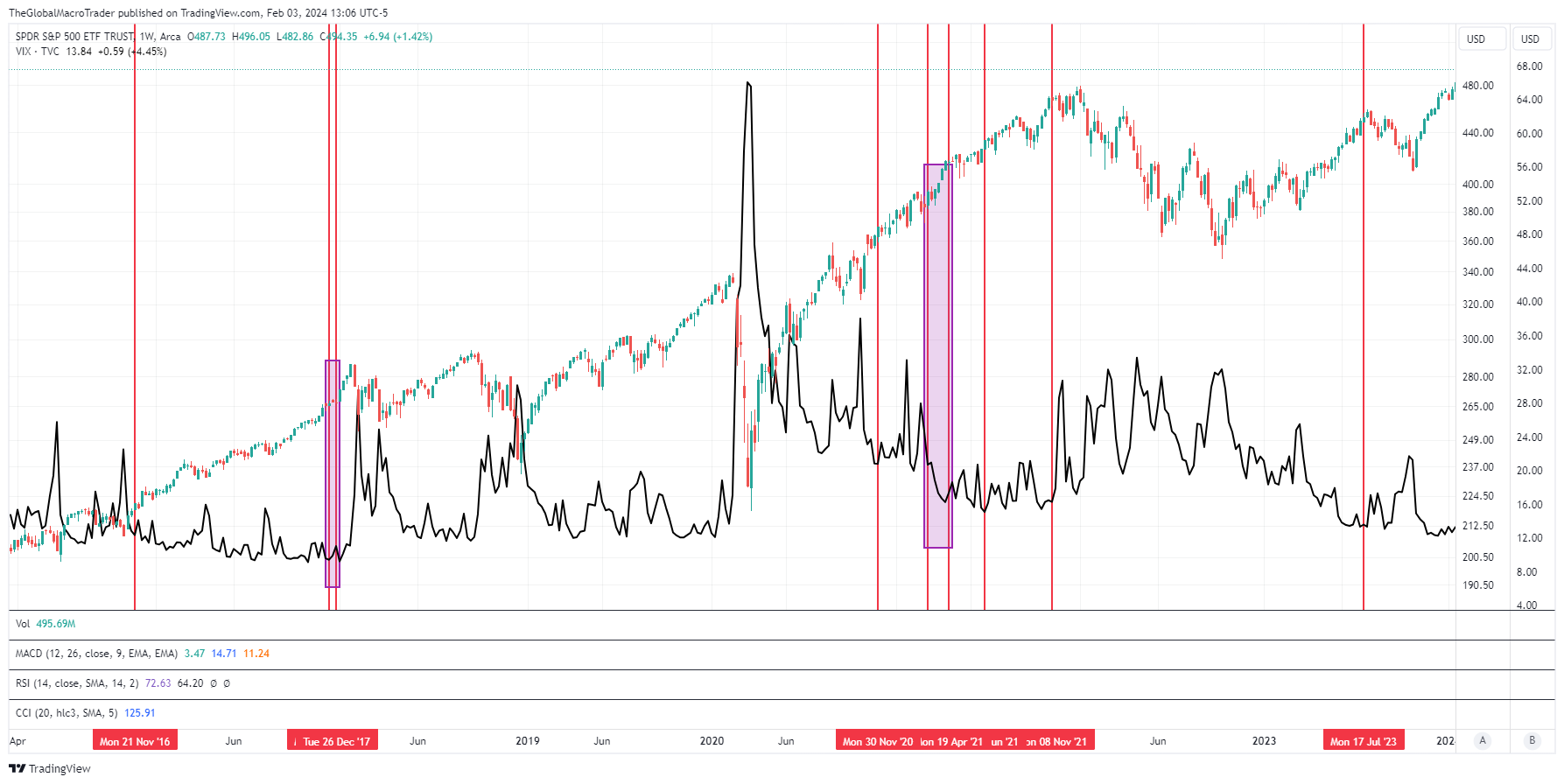

Here is a chart of the SPY ETF along with vertical lines corresponding to those high bullish periods. I added the shaded rectangles to indicate multiple weeks of bullishness.

I would never trade based off this data of course, but it is an indication of how investors are feeling about the market - very bullish. Now, this also is important when considering that any miss in terms of expectations will be hit hard.

One way I am thinking about these periods in the past is that they were accompanied by low volatility, as indicated on the chart with the VIX (black line). This means that buying insurance through options is relatively cheap. Looking out approximately three months from the peak bullish periods, a number of these periods experienced at least some increase in volatility. I have been doing so with several of my portfolios, using various option techniques to add some hedges to the downside.

China

China is in freefall. I wrote at the beginning of the year that I am interested in watching China, specifically if the authorities implement significant structural changes that may create at least a short-term trading bottom. Well, the market is firmly saying no, there is a lot more to do in China than meets the eye.

This is the monthly chart of iShares China Large Cap ETF FXI (candlesticks) and the Kraneshares Trust CSI China ETF KWEB (orange line). Terrible looking charts. If someone bought the FXI in 2005, they would essentially be flat today.

We all know that China has some serious headwinds, including demographics, but I thought that perhaps the Chinese authorities may open the spigot to help their economy especially given the property market crash.

There have been some actions taken, such as stopping shares being lent out for short selling. The National Administration of Financial Regulation announced changes that they hope will expand commercial loans by banks to property developers, including adjusting repayment terms. The deputy head Xiao Yuanqi stated (article here), “[We will] ask banks to take action as soon as possible... [and] make good use of the policy toolbox and accurately support the reasonable financing needs of real estate projects.”

The PBOC added 1 trillion yuan of liquidity by cutting the reserve requirement ration by 50bps.

More measures came out permitting developers to use commercial property loans to pay off other debt. There are also reports of that the Chinese may use 2 trillion yuan from offshore state-owned firms to buy shares onshore

There are other measures that I have not included, but in short their economy and markets are a mess. Given the massive overhang of debt related to the property crash, the drop in property prices and now the feeling that these efforts are just not enough, I think it is still quite dangerous to even dip my toe in the water. I am tempted, but I will wait until I see evidence of structural changes that will put a floor down before entering the market. We will also see buyers start to re-enter the market and therefore prices start moving higher. Long-term I think China has some massive problems, but I think at some point this year the Chinese authorities will have to go all-in and really show the market and their people that they are serious about changes to benefit the economy and the markets.

What to Watch This Week

This week is relatively light for data in the US

On Monday the Fed updates its Senior Loan Officer Survey. So far the level of tightening lending standards has not been as feared, but this will be an important area to watch given how much this can directly affect the economy.

PMI data out Monday along with ISM services

Auctions

$54bn 3 year Tuesday

$42bn 10 year Wednesday

$25bn 30 year Thursday

Plenty of Fed speakers! Let’s see if they have a different take than Chair Powell. I think all will say that they are watching the labor market closely, especially after the strong print on Friday.

Speakers includes Mester, Kashkari, Harker, Kugler, Barkin and Bowman

Equities

I wrote last week, “I still hold a position in the S&P 500 (this is the SPX index) from 4400 area (see prior weeks for more info). I am moving my stops further higher in the 4830-4840 area.” The SPX came close, down to 4845, but then rebounded strongly higher.

As I pointed out last week, the S&P 500 was at a point of inflection - clearly the choice is higher (at least for now).

If momentum starts to regain, we could be setting up for a move towards 5300 or so.

As I discussed earlier, volatility is low and I think it is a good idea to add some hedges. I have done so with my long-term portfolios, including options combinations to add downside protection without too much cost.

Not much in terms of economic news this week to be of concern for bulls, but perhaps some of the Fed commentators will try to add some cold water to the equity rally. Also earnings season has been very strong for tech firms and energy, there could always be issues with firms coming out this week.

For the time being the short-term trade remains to be bullish equities.

Fixed Income

All yields backed up Friday following the strong jobs data.

The question I ask myself, are we about to see the economy re-accelerate strongly? One data print is not enough, in terms of jobs. Also the inflation picture continues to improve, although as I previously pointed out that it is not necessarily smooth sailing either. There are risks, but I think the Fed is taking the right approach, they seem firmly committed to squeezing inflation out of the system. This, in my opinion, increases that they will squeeze too hard and the economy will contract. That would result in 1) inflation continuing to decrease, and 2) Fed cuts larger than expected to counteract an economic recession, even if mild.

This chart is the monthly 10 year yield along with the Fed funds rate (blue line) and at the bottom the q/q change in the PCE index.

First, 10 year yields have moved up a massive amount. Not just in relation to the covid pandemic, but even to other recent periods such as 2018 when yields ranged from the (approximate) 2.7-3.2%ish levels.

Can yields move higher? Of course, and I can see this possible even this week with a concession for the 10 year auction, but I think there are limits to the upside in yields - unless inflation and the economy pick up steam. I think 4.25% is quite possible, but 5% being a very low probability event (unless the fundamentals change dramatically).

As I said last week, “I think we will see at least 3.50% at some point this year. I continue to look at trading ranges in the 10 year, buying in the 4.10-4.20% and looking to trim around 3.80%. I think there will be a few oscillations back and forth this year.”

While I do trade the futures, I also have long-term retirement accounts and in those I am using an instrument like the TLT to hold and writing out of the money call options to generate some additional yield. I don’t think the first half of 2024 will be any large movements up or down, just range bound trading and therefore harvesting options premium is a logical move (in my opinion).

Oil

Oil pulled back sharply last week. A lot of volatility in the market and difficult to get a clear picture and edge. The war situation, Red Sea, weather outages causing US producers to curb production and so on. I see no edge and no attractive risk:reward - I remain on the sidelines.

Gold

Gold popped much higher last week. US dollar strength at the end of the week looks to have taken the momentum out of the gold market, but I am becoming very interested. I would want to see gold hold above $2020 or so for a few days and I would enter a small long. I would then add as gold moved through $2070-$2080.

Thanks for reading!

theglobalmacrotrader@gmail.com

Twitter —> @TheGlobalMacro

Disclaimer

Copyright (c) TheGlobalMacroTrader.com 2024. All rights reserved. All material presented either through the TheGlobalMacroTrader.com website, Substack, any newsletter published by this site, posts on any social media platform and other public comments are not to be regarded as investment advice, but for general informational and entertainment purposes only. You, the reader, assume the entire cost and risk of any trading you choose to undertake. You, the reader, are solely responsible for making your own investment decisions. Owners of this newsletter, its representatives, its principals, are NOT registered as securities broker-dealers or investment advisors either with the U.S. Securities and Exchange Commission or with any securities regulatory authority. We recommend consulting with a registered investment advisor, broker-dealer, and/or financial advisor. If you choose to invest with or without seeking advice from such an advisor or entity, then any consequences resulting from your investments are your sole responsibility. Reading and using this newsletter or using our content on the web/server, you are indicating your consent and agreement to our disclaimer. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice and are for entertainment purposes only, no advice has been presented and no recommendation have been made. All information on TheGlobalMacroTrader.com, and any associated pages such as the SubStack pages, are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings along with discussion over chart formations and quantitative metrics may be mentioned but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security—including commodities, currencies, stocks, bonds, exchange traded funds (ETF), exchange traded notes (ETN), mutual funds, futures contracts, or any similar instruments. All text, images, ideas and concepts on TheGlobalMacroTrader.com and associated websites, emails, posts and social media messages constitute valuable intellectual property. No material from any part of TheGlobalMacroTrader.com and associated websites, emails, posts and messages may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of TheGlobalMacroTrader.com. All unauthorized reproduction or other use of material from TheGlobalMacroTrader.com and associated websites, pages and emails shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. The recipient should check any email and any attachments for the presence of viruses. TheGlobalMacroTrader.com accepts no liability for any damage caused by any virus transmitted by this company’s website, emails, attachments, posts and any other method of communication. TheGlobalMacroTrader.com expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. TheGlobalMacroTrader.com reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.